|

Front-end and Back-end Segments Projected to Support Consecutive Growth from 2024 through 2026

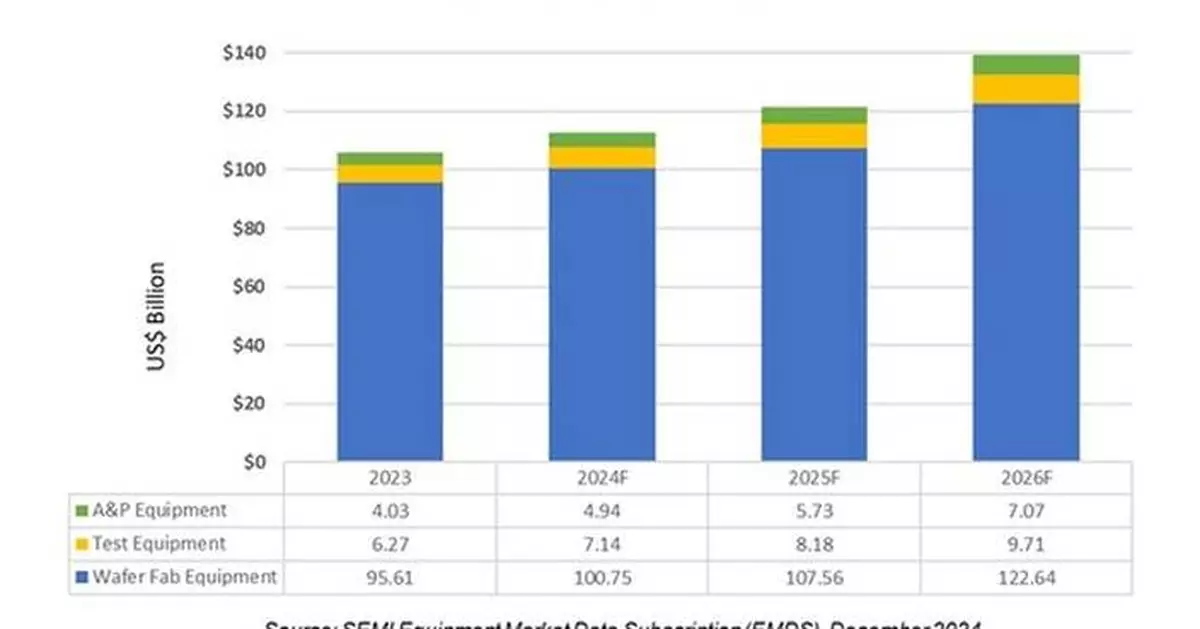

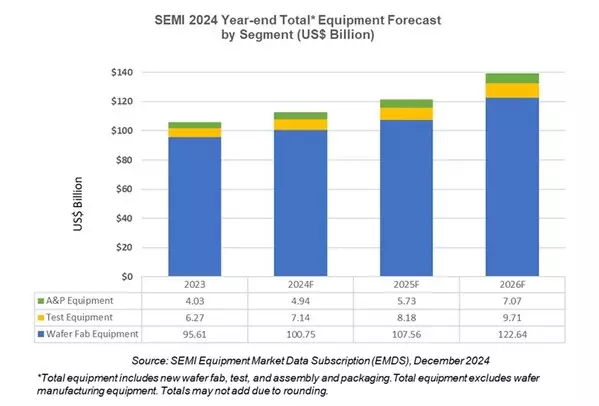

TOKYO, Dec. 9, 2024 /PRNewswire/ -- Global sales of total semiconductor manufacturing equipment by original equipment manufacturers (OEMs) are forecast to set a new industry record, reaching $113 billion in 2024, growing 6.5% year-on-year, SEMI announced today in its Year-End Total Semiconductor Equipment Forecast – OEM Perspective at SEMICON Japan 2024. Semiconductor manufacturing equipment growth is expected to continue in the following years, reaching new records of $121 billion in 2025 and $139 billion in 2026, supported by both the front-end and back-end segments.

"Three consecutive years of projected growth in investments in semiconductor manufacturing reflect the vital role our industry plays in underpinning the global economy and advancing technology innovation," said Ajit Manocha, SEMI president and CEO. "Since our July 2024 forecast, the outlook for 2024 semiconductor equipment sales has brightened, especially with stronger-than-expected investments from China and in AI-related sectors. Together with our forecast extension through 2026, it highlights the robust growth drivers across segments, applications, and regions."

Semiconductor Equipment Sales by Segment

After registering a record $96 billion in sales last year, the wafer fab equipment (WFE) segment, which includes wafer processing, mask/reticle, and fab facilities equipment, is projected to grow 5.4% to $101 billion in 2024. This marks an increase from the previously forecast $98 billion in SEMI's 2024 Mid-Year Equipment Forecast. The upward revision mainly reflects the ongoing strong equipment investments in DRAM and high-bandwidth memory (HBM) driven by artificial intelligence (AI) computing. Additionally, China's investments continue to play a significant role in the WFE market expansion. Looking ahead, WFE segment sales are projected to expand 6.8% in 2025 and 14% in 2026, reaching $123 billion due to increased demand for advanced logic and memory applications.

Following two years of contraction, the back-end equipment segment in 2024 saw a strong recovery in particular in the second half of the year. Sales of semiconductor test equipment are projected to rise 13.8% to $7.1 billion in 2024, while assembly and packaging (A&P) equipment sales are projected to increase 22.6% to $4.9 billion. Furthermore, the back-end segment growth is expected to accelerate, with test equipment sales surging 14.7% in 2025 and 18.6% in 2026, respectively, while A&P sales are forecast to grow 16% in 2025 followed by 23.5% expansion in 2026. The back-end segments' growth is supported by the increasing complexity of semiconductor devices for high-performance computing and the expected increase in demand in the mobile, automotive, and industrial end-markets.

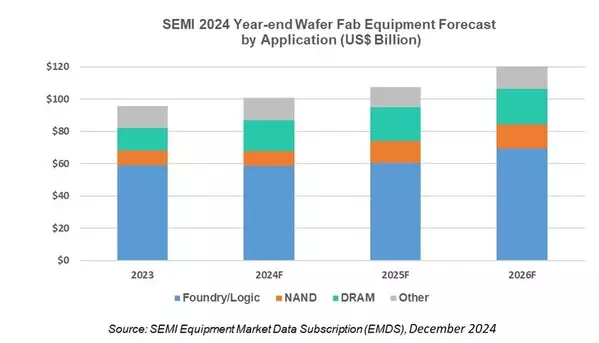

Wafer Fab Equipment Sales by Application

The sales of WFE for foundry and logic applications are expected to remain flat year-on-year at $58.6 billion in 2024, supported by resilient spending in mature nodes. The segment is forecast to see 2.8% growth in 2025 and to increase 15% to $69.3 billion in 2026, driven by increasing demand for leading-edge technology, the introduction of new device architectures including the transition to gate-all-around (GAA), and increased capacity expansion purchases.

Memory-related capital expenditures are projected to see significant increases through 2026 supported by increasing demand for HBM for AI deployment and ongoing technology migration. NAND equipment sales are expected to remain relatively soft in 2024, growing 0.7% to $9.3 billion as supply and demand continues to normalize, setting the stage for a 47.8% expansion to $13.7 billion in 2025 and 9.7% growth to $15.1 billion in 2026. Meanwhile, DRAM equipment sales are projected to see robust growth of 35.3% to $18.8 billion in 2024, followed by 10.4% and 6.2% year-on-year growth in 2025 and 2026, respectively.

Semiconductor Equipment Sales by Region

Mainland China, Taiwan and Korea are expected to remain the top three destinations for equipment spending through 2026. China is projected to maintain the top position over the forecast period as the region's equipment purchases continue to remain resilient despite the anticipated slowdown. Equipment shipments to China are projected to reach a record $49 billion in 2024, solidifying its lead over other regions. While equipment spending for most regions is expected to fall in 2024 before rebounding in 2025, China is expected to see a contraction in 2025 following significant investments over the past three years. All regions tracked are expected to see increases in 2026.

The SEMI forecast is based on collective input from top equipment suppliers, the SEMI Worldwide Semiconductor Equipment Market Statistics (WWSEMS) data collection program and the industry-recognized SEMI World Fab Forecast database.

About SEMI Market Data

The Equipment Market Data Subscription (EMDS) from SEMI provides comprehensive market data for the global semiconductor equipment market. A subscription includes three reports:

- Monthly SEMI North American Billings Report, an early perspective of equipment market trends

- Monthly Worldwide Semiconductor Equipment Market Statistics (WWSEMS), a detailed report of semiconductor equipment billings for seven regions and more than 22 market segments

- Bi-annual Total Semiconductor Equipment Forecast – OEM Perspective, an outlook for the semiconductor equipment market

For more information online, please visit SEMI Market Data.

About SEMI

SEMI® is the global industry association connecting over 3,000 member companies and 1.5 million professionals worldwide across the semiconductor and electronics design and manufacturing supply chain. We accelerate member collaboration on solutions to top industry challenges through Advocacy, Workforce Development, Sustainability, Supply Chain Management and other programs. Our SEMICON® expositions and events, technology communities, standards and market intelligence help advance our members' business growth and innovations in design, devices, equipment, materials, services and software, enabling smarter, faster, more secure electronics. Visit www.semi.org, contact a regional office, and connect with SEMI on LinkedIn and X to learn more.

Association Contact

Samer Bahou/SEMI

Phone: 1.408.943.7870

Email: sbahou@semi.org

Front-end and Back-end Segments Projected to Support Consecutive Growth from 2024 through 2026

TOKYO, Dec. 9, 2024 /PRNewswire/ -- Global sales of total semiconductor manufacturing equipment by original equipment manufacturers (OEMs) are forecast to set a new industry record, reaching $113 billion in 2024, growing 6.5% year-on-year, SEMI announced today in its Year-End Total Semiconductor Equipment Forecast – OEM Perspective at SEMICON Japan 2024. Semiconductor manufacturing equipment growth is expected to continue in the following years, reaching new records of $121 billion in 2025 and $139 billion in 2026, supported by both the front-end and back-end segments.

"Three consecutive years of projected growth in investments in semiconductor manufacturing reflect the vital role our industry plays in underpinning the global economy and advancing technology innovation," said Ajit Manocha, SEMI president and CEO. "Since our July 2024 forecast, the outlook for 2024 semiconductor equipment sales has brightened, especially with stronger-than-expected investments from China and in AI-related sectors. Together with our forecast extension through 2026, it highlights the robust growth drivers across segments, applications, and regions."

Semiconductor Equipment Sales by Segment

After registering a record $96 billion in sales last year, the wafer fab equipment (WFE) segment, which includes wafer processing, mask/reticle, and fab facilities equipment, is projected to grow 5.4% to $101 billion in 2024. This marks an increase from the previously forecast $98 billion in SEMI's 2024 Mid-Year Equipment Forecast. The upward revision mainly reflects the ongoing strong equipment investments in DRAM and high-bandwidth memory (HBM) driven by artificial intelligence (AI) computing. Additionally, China's investments continue to play a significant role in the WFE market expansion. Looking ahead, WFE segment sales are projected to expand 6.8% in 2025 and 14% in 2026, reaching $123 billion due to increased demand for advanced logic and memory applications.

Following two years of contraction, the back-end equipment segment in 2024 saw a strong recovery in particular in the second half of the year. Sales of semiconductor test equipment are projected to rise 13.8% to $7.1 billion in 2024, while assembly and packaging (A&P) equipment sales are projected to increase 22.6% to $4.9 billion. Furthermore, the back-end segment growth is expected to accelerate, with test equipment sales surging 14.7% in 2025 and 18.6% in 2026, respectively, while A&P sales are forecast to grow 16% in 2025 followed by 23.5% expansion in 2026. The back-end segments' growth is supported by the increasing complexity of semiconductor devices for high-performance computing and the expected increase in demand in the mobile, automotive, and industrial end-markets.

Wafer Fab Equipment Sales by Application

The sales of WFE for foundry and logic applications are expected to remain flat year-on-year at $58.6 billion in 2024, supported by resilient spending in mature nodes. The segment is forecast to see 2.8% growth in 2025 and to increase 15% to $69.3 billion in 2026, driven by increasing demand for leading-edge technology, the introduction of new device architectures including the transition to gate-all-around (GAA), and increased capacity expansion purchases.

Memory-related capital expenditures are projected to see significant increases through 2026 supported by increasing demand for HBM for AI deployment and ongoing technology migration. NAND equipment sales are expected to remain relatively soft in 2024, growing 0.7% to $9.3 billion as supply and demand continues to normalize, setting the stage for a 47.8% expansion to $13.7 billion in 2025 and 9.7% growth to $15.1 billion in 2026. Meanwhile, DRAM equipment sales are projected to see robust growth of 35.3% to $18.8 billion in 2024, followed by 10.4% and 6.2% year-on-year growth in 2025 and 2026, respectively.

Semiconductor Equipment Sales by Region

Mainland China, Taiwan and Korea are expected to remain the top three destinations for equipment spending through 2026. China is projected to maintain the top position over the forecast period as the region's equipment purchases continue to remain resilient despite the anticipated slowdown. Equipment shipments to China are projected to reach a record $49 billion in 2024, solidifying its lead over other regions. While equipment spending for most regions is expected to fall in 2024 before rebounding in 2025, China is expected to see a contraction in 2025 following significant investments over the past three years. All regions tracked are expected to see increases in 2026.

The SEMI forecast is based on collective input from top equipment suppliers, the SEMI Worldwide Semiconductor Equipment Market Statistics (WWSEMS) data collection program and the industry-recognized SEMI World Fab Forecast database.

About SEMI Market Data

The Equipment Market Data Subscription (EMDS) from SEMI provides comprehensive market data for the global semiconductor equipment market. A subscription includes three reports:

- Monthly SEMI North American Billings Report, an early perspective of equipment market trends

- Monthly Worldwide Semiconductor Equipment Market Statistics (WWSEMS), a detailed report of semiconductor equipment billings for seven regions and more than 22 market segments

- Bi-annual Total Semiconductor Equipment Forecast – OEM Perspective, an outlook for the semiconductor equipment market

For more information online, please visit SEMI Market Data.

About SEMI

SEMI® is the global industry association connecting over 3,000 member companies and 1.5 million professionals worldwide across the semiconductor and electronics design and manufacturing supply chain. We accelerate member collaboration on solutions to top industry challenges through Advocacy, Workforce Development, Sustainability, Supply Chain Management and other programs. Our SEMICON® expositions and events, technology communities, standards and market intelligence help advance our members' business growth and innovations in design, devices, equipment, materials, services and software, enabling smarter, faster, more secure electronics. Visit www.semi.org, contact a regional office, and connect with SEMI on LinkedIn and X to learn more.

Association Contact

Samer Bahou/SEMI

Phone: 1.408.943.7870

Email: sbahou@semi.org

** The press release content is from PR Newswire. Bastille Post is not involved in its creation. **

Global Total Semiconductor Equipment Sales Forecast to Reach a Record of $139 Billion in 2026, SEMI Reports

Global Total Semiconductor Equipment Sales Forecast to Reach a Record of $139 Billion in 2026, SEMI Reports

|

Across three sessions in Dubai this spring, the conversations moved from how AI agents are built and reshaping business operations to whether the market's pricing of the build-out can hold.

DUBAI, UAE, May 22, 2026 /PRNewswire/ -- Peter Karsten, CEO of STARTRADER, joined the University of Europe for Applied Sciences in One Central, Dubai, for three separate sessions this spring; two with MBA Operations students led by Prof. Dr. Katariina Juusola, and a third hosted by Prof. Dr. Eman AbuKhousa;each drawing students, faculty members, and finance professionals into extended conversations that ran past their scheduled close.

MBA Operations: 25 April and 9 May

The first MBA session, on 25 April, introduced students to the rapidly evolving world of AI, autonomous systems, and the future of business operations. Drawing from extensive international industry experience, Karsten covered autonomous AI agents and multi-agent systems, AI-driven decision-making, distributed computing infrastructure, human–AI collaboration, and the cybersecurity and governance risks that come with the shift.

One of the most memorable moments came through what Karsten called the "chainsaw metaphor"; comparing traditional business tools and workflows to a manual saw, with AI as the chainsaw: dramatically more powerful and faster, but requiring entirely new ways of working, thinking, and managing risk.

The second MBA session, on 9 May, went deeper into AI agents, distributed systems, and the transformative impact these technologies are expected to have on organisations and society. A recurring theme across both sessions was the idea that the world has already changed — organisations are now racing to adapt to a new operational reality shaped by AI, not preparing for one that might arrive.

Market Risk and Valuation: 15 May

The third session shifted to the market implications. Titled "AI Investment, Productivity Lag & Valuation Risk," it tackled one of the debates that has been splitting opinion across markets for months. Trillions in AI-related capital expenditure, yet the productivity gains haven't shown up clearly in the macro data. At the same time, valuations on a handful of AI-exposed names sit at levels that have strategists watching closely for parallels to past cycles.

Karsten pushed back on both ends. The capex is real, he argued, and dismissing it as a bubble underestimates how foundational this infrastructure build-out is. But he was just as direct on the risk side: when valuation gaps correct, they tend to do so faster than retail investors expect.

"The productivity gains are coming. The question is whether they arrive before the market loses patience," he said during the Q&A. "That gap, between what's being spent and what's showing up in the numbers, is where the real risk sits right now."

"Sessions like this give our students direct exposure to how industry leaders are thinking about the risks and opportunities in AI right now," said Prof. Dr. Eman AbuKhousa, Professor of AI & Data Science, who teaches in the university's Software Engineering programme. "That kind of real-world perspective is difficult to replicate in a classroom, and it's exactly the sort of dialogue we want more of."

jwplayer.key="3Fznr2BGJZtpwZmA+81lm048ks6+0NjLXyDdsO2YkfE="

STARTRADER CEO Peter Karsten Joins University of Europe for Three Sessions Spanning AI Infrastructure, Business Operations, and Market Risk jwplayer('myplayer1').setup({file: 'https://mma.prnasia.com/media2/2986082/STARTRADER.mp4', image: 'https://mma.prnasia.com/media2/2986082/STARTRADER.mp4?p=thumbnail', autostart:'false', stretching : 'uniform', width: '512', height: '288'});

A Broader Commitment

STARTRADER's involvement reflects its broader commitment to financial education, particularly where emerging technologies are reshaping how markets operate.

Both STARTRADER and the University of Europe for Applied Sciences share a belief that sound decision-making depends on understanding the mechanics behind the narrative. The university prepares students across its Business, Data Science, and Software Engineering programmes to enter a technology-driven landscape; STARTRADER operates within it daily, making the exchange a natural one.

The partnership with the University of Europe marks STARTRADER's second public university engagement of the year, following an online keynote at the University of Adelaide in January. The company plans to continue joining academic and industry-led discussions through the rest of 2026, with AI adoption, valuation pressure, and macroeconomic uncertainty expected to remain front and centre across global markets.

Beyond the broader market conversation, these engagements serve a direct purpose for STARTRADER: building meaningful connections with the next generation of finance and trading professionals at the moment they are forming their view of the industry.

About STARTRADER

STARTRADER is a global multi-asset broker empowering retail and institutional partners to access global markets through a range of platforms, including MetaTrader, STAR-APP, and STAR-COPY.

Regulated across five jurisdictions (CMA, ASIC, FSCA, FSA, and FSC), STARTRADER combines strong governance with a client-first approach, serving both retail clients and partners with a commitment to transparency, reliability, and long-term growth.

Across three sessions in Dubai this spring, the conversations moved from how AI agents are built and reshaping business operations to whether the market's pricing of the build-out can hold.

DUBAI, UAE, May 22, 2026 /PRNewswire/ -- Peter Karsten, CEO of STARTRADER, joined the University of Europe for Applied Sciences in One Central, Dubai, for three separate sessions this spring; two with MBA Operations students led by Prof. Dr. Katariina Juusola, and a third hosted by Prof. Dr. Eman AbuKhousa;each drawing students, faculty members, and finance professionals into extended conversations that ran past their scheduled close.

MBA Operations: 25 April and 9 May

The first MBA session, on 25 April, introduced students to the rapidly evolving world of AI, autonomous systems, and the future of business operations. Drawing from extensive international industry experience, Karsten covered autonomous AI agents and multi-agent systems, AI-driven decision-making, distributed computing infrastructure, human–AI collaboration, and the cybersecurity and governance risks that come with the shift.

One of the most memorable moments came through what Karsten called the "chainsaw metaphor"; comparing traditional business tools and workflows to a manual saw, with AI as the chainsaw: dramatically more powerful and faster, but requiring entirely new ways of working, thinking, and managing risk.

The second MBA session, on 9 May, went deeper into AI agents, distributed systems, and the transformative impact these technologies are expected to have on organisations and society. A recurring theme across both sessions was the idea that the world has already changed — organisations are now racing to adapt to a new operational reality shaped by AI, not preparing for one that might arrive.

Market Risk and Valuation: 15 May

The third session shifted to the market implications. Titled "AI Investment, Productivity Lag & Valuation Risk," it tackled one of the debates that has been splitting opinion across markets for months. Trillions in AI-related capital expenditure, yet the productivity gains haven't shown up clearly in the macro data. At the same time, valuations on a handful of AI-exposed names sit at levels that have strategists watching closely for parallels to past cycles.

Karsten pushed back on both ends. The capex is real, he argued, and dismissing it as a bubble underestimates how foundational this infrastructure build-out is. But he was just as direct on the risk side: when valuation gaps correct, they tend to do so faster than retail investors expect.

"The productivity gains are coming. The question is whether they arrive before the market loses patience," he said during the Q&A. "That gap, between what's being spent and what's showing up in the numbers, is where the real risk sits right now."

"Sessions like this give our students direct exposure to how industry leaders are thinking about the risks and opportunities in AI right now," said Prof. Dr. Eman AbuKhousa, Professor of AI & Data Science, who teaches in the university's Software Engineering programme. "That kind of real-world perspective is difficult to replicate in a classroom, and it's exactly the sort of dialogue we want more of."

STARTRADER CEO Peter Karsten Joins University of Europe for Three Sessions Spanning AI Infrastructure, Business Operations, and Market Risk jwplayer('myplayer1').setup({file: 'https://mma.prnasia.com/media2/2986082/STARTRADER.mp4', image: 'https://mma.prnasia.com/media2/2986082/STARTRADER.mp4?p=thumbnail', autostart:'false', stretching : 'uniform', width: '512', height: '288'});

A Broader Commitment

STARTRADER's involvement reflects its broader commitment to financial education, particularly where emerging technologies are reshaping how markets operate.

Both STARTRADER and the University of Europe for Applied Sciences share a belief that sound decision-making depends on understanding the mechanics behind the narrative. The university prepares students across its Business, Data Science, and Software Engineering programmes to enter a technology-driven landscape; STARTRADER operates within it daily, making the exchange a natural one.

The partnership with the University of Europe marks STARTRADER's second public university engagement of the year, following an online keynote at the University of Adelaide in January. The company plans to continue joining academic and industry-led discussions through the rest of 2026, with AI adoption, valuation pressure, and macroeconomic uncertainty expected to remain front and centre across global markets.

Beyond the broader market conversation, these engagements serve a direct purpose for STARTRADER: building meaningful connections with the next generation of finance and trading professionals at the moment they are forming their view of the industry.

About STARTRADER

STARTRADER is a global multi-asset broker empowering retail and institutional partners to access global markets through a range of platforms, including MetaTrader, STAR-APP, and STAR-COPY.

Regulated across five jurisdictions (CMA, ASIC, FSCA, FSA, and FSC), STARTRADER combines strong governance with a client-first approach, serving both retail clients and partners with a commitment to transparency, reliability, and long-term growth.

** This press release is distributed by PR Newswire through automated distribution system, for which the client assumes full responsibility. **

STARTRADER CEO Peter Karsten Joins University of Europe for Three Sessions Spanning AI Infrastructure, Business Operations, and Market Risk

STARTRADER CEO Peter Karsten Joins University of Europe for Three Sessions Spanning AI Infrastructure, Business Operations, and Market Risk