Economic performance in first quarter of 2026 and latest GDP and price forecasts for 2026

The Government released today (May 15) the First Quarter Economic Report 2026, together with the revised figures on Gross Domestic Product (GDP) for the first quarter of 2026.

Click to Gallery

Source: HKSAR Government Press Releases

Source: HKSAR Government Press Releases

Source: HKSAR Government Press Releases

The Government Economist, Ms Irina Fan (centre), presents the First Quarter Economic Report 2026 at a press conference today (May 15). Also present are Principal Economist Mr Eric Lee (left) and Assistant Commissioner for Census and Statistics Ms Edith Chan (right). Source: HKSAR Government Press Releases

The Government Economist, Ms Irina Fan, gave an account of the economic performance in the first quarter of 2026 and the latest GDP and price forecasts for 2026.

Main points

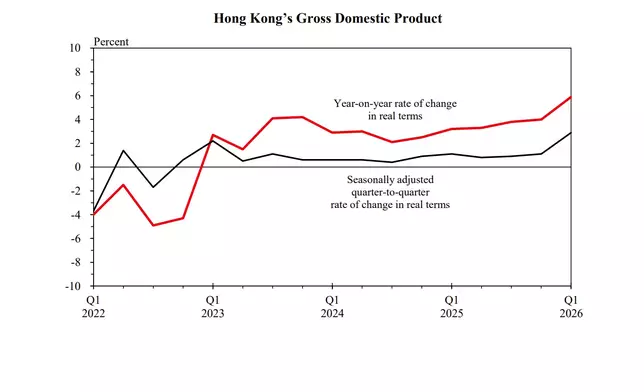

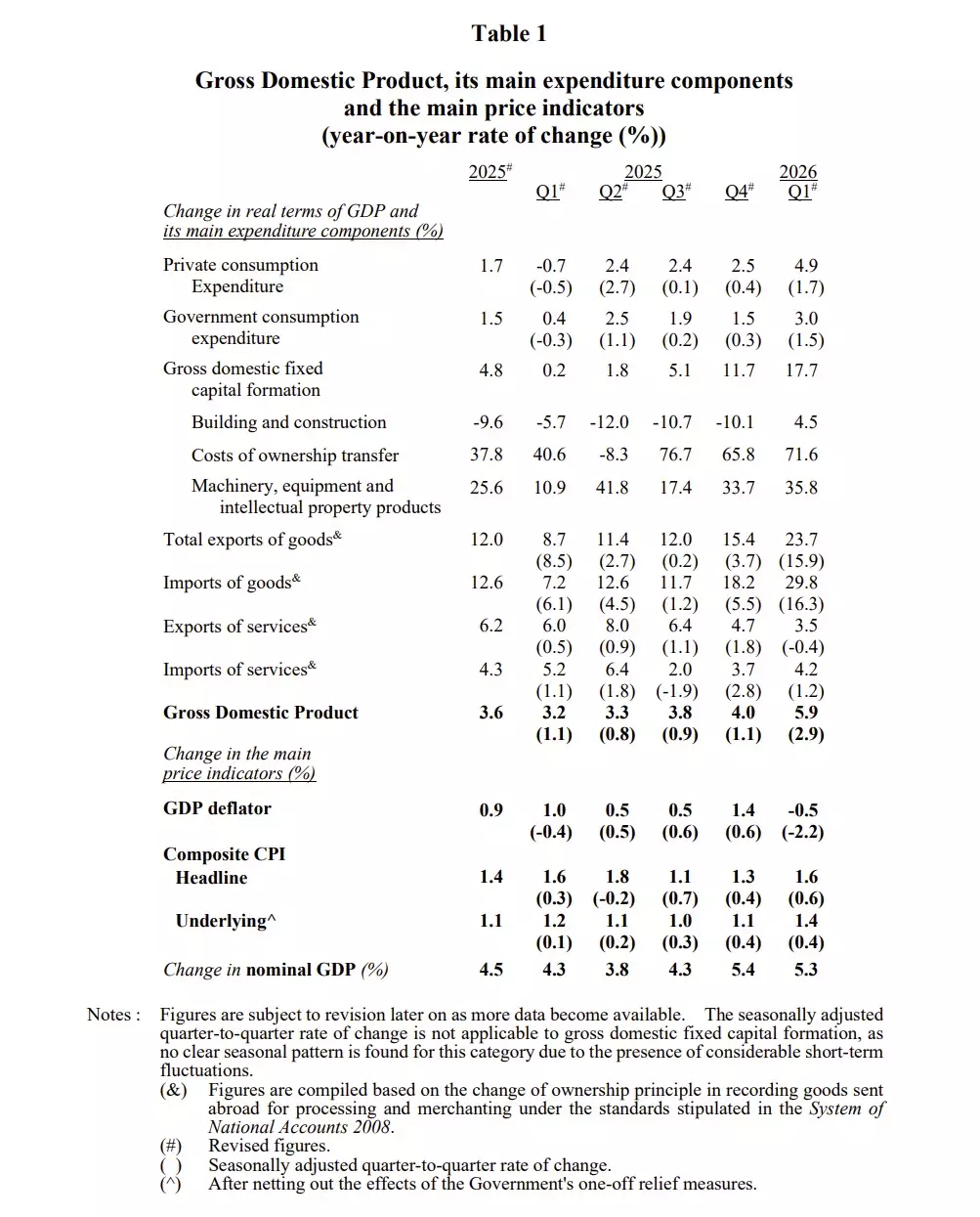

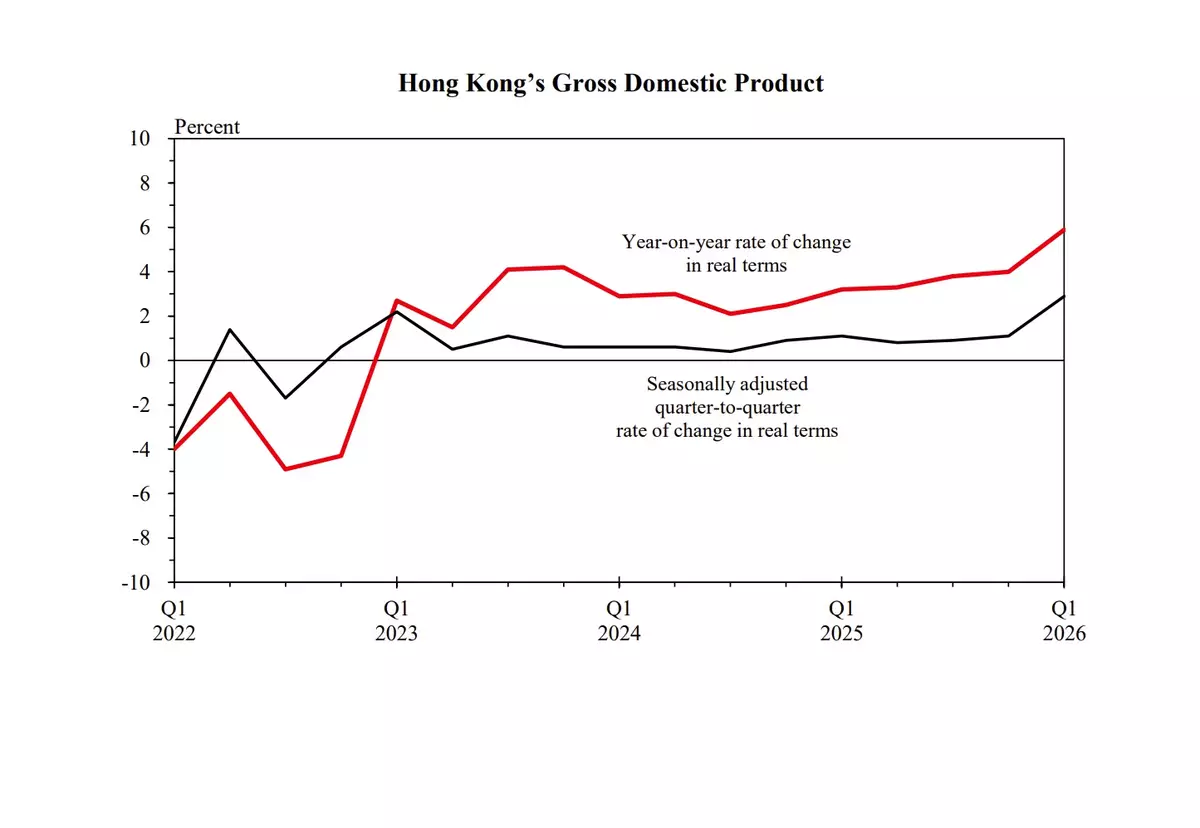

The Hong Kong economy expanded robustly in the first quarter of 2026, driven by the sustained strong performance in external trade and pick-up in domestic demand. Real GDP grew by 5.9% over a year earlier in the first quarter, accelerating from the 4.0% growth in the preceding quarter. On a seasonally adjusted quarter-to-quarter comparison, real GDP rose notably by 2.9%.

Total exports of goods grew markedly by 23.7% year-on-year in real terms in the first quarter, underpinned by sustained global demand for artificial intelligence (AI)-related electronic products and buoyant regional trade flows in Asia. Exports of services continued to expand solidly by 3.5% in real terms over a year earlier, with broad-based growth across all major service groups.

Domestic demand strengthened across both consumption and investment. Private consumption expenditure saw accelerated growth of 4.9% year-on-year in real terms in the first quarter, reflecting the more entrenched recovery in households' spending. Overall investment expenditure continued to expand at a double-digit rate of 17.7% year-on-year in real terms in the first quarter, alongside the robust economic growth.

The labour market showed modest improvement in the first quarter. The seasonally adjusted unemployment rate edged down further by 0.1 percentage point from the preceding quarter to 3.7% in the first quarter. The underemployment rate also decreased by 0.1 percentage point to 1.6%. Average employment earnings continued to record year-on-year growth in the first quarter.

The local stock market saw varying monthly performance during the first quarter. The Hang Seng Index (HSI) rallied to a four-and-a-half-year high of nearly 28 000 in January, moved sideways in February, and corrected in March after the Middle East conflict. Trading and fundraising activities remained strong throughout the quarter. More lately, since entering the second quarter, the HSI has largely recovered the earlier lost ground and returned to the pre-conflict levels. Separately, the residential property market continued to strengthen in the first quarter, with both prices and rentals recording further increases.

Consumer price inflation stayed modest in the first quarter, though it picked up somewhat in March, mainly driven by fuel-related components amid higher international oil prices. Price pressures in other components were largely contained. The underlying Composite Consumer Price Index (Composite CPI) rose by 1.4% in the first quarter over a year earlier, following the 1.1% increase in the preceding quarter.

Looking ahead, Hong Kong's economic outlook remains broadly resilient. Strong global demand for advanced electronics and AIrelated products is expected to support goods export performance, while services exports should remain firm, underpinned by sustained vibrancy in inbound tourism, robust cross-boundary financial activity, and steady demand for business services. Relatively solid consumer sentiment and resilient business outlook are expected to support domestic demand. The impacts of the Middle East conflict on the Hong Kong economy have so far been limited. Yet, the outlook of the conflict remains highly uncertain. A further escalation or persistence of tensions could heighten global financial market volatility, posing downside risks to growth and upside risks to inflation.

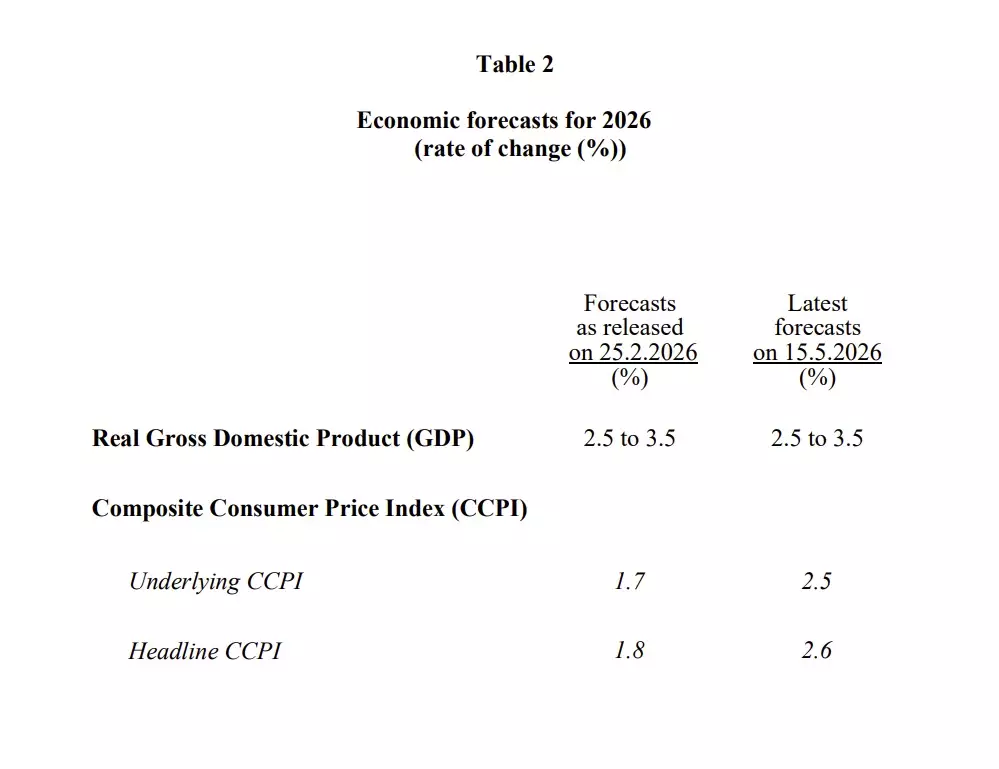

Taking into account the stronger-than-expected outturn in the first quarter and the potential near-term headwinds in the external environment, the real GDP growth forecast for 2026 as a whole is maintained at 2.5% – 3.5%, the same as that announced in the Budget. Risk to growth is tilted to the downside due to the uncertainty surrounding the actual outcome of the scale and duration of the Middle East conflict.

On the inflation outlook, the feed-through of higher international oil prices to fuel-related components in consumer prices should continue in the coming months. Overall inflation in Hong Kong is, however, expected to remain relatively well anchored, reflecting the city's low energy intensity as a predominantly service-oriented economy, with stable energy supplies from the Chinese Mainland (Mainland) helping to mitigate external shocks. Taking into account the actual inflation situation in the first quarter and the factors mentioned above, the forecasts for the underlying and headline consumer price inflation rates for 2026 are revised up to 2.5% and 2.6% respectively, from 1.7% and 1.8% as announced in the Budget.

In the past two months, the Government has introduced short-term, targeted measures to provide timely relief to sectors with relatively high fuel cost. The Government remains vigilant to the risks of further escalation of the conflict, will closely monitor the developments, and will respond further as appropriate to safeguard price stability.

Details

GDP

According to the revised figures released today by the Census and Statistics Department, real GDP grew robustly by 5.9% year-on-year in the first quarter of 2026 (same as the advance estimate), having increased by 4.0% in the preceding quarter. On a seasonally adjusted quarter-to-quarter comparison, real GDP rose by 2.9% in the first quarter (same as the advance estimate), further to the 1.1% increase in the preceding quarter (Chart).

Source: HKSAR Government Press Releases

The latest figures on GDP and its major expenditure components up to the first quarter of 2026 are presented in Table 1. Developments in different segments of the economy in the first quarter are described below.

Source: HKSAR Government Press Releases

External trade

Total exports of goods grew markedly by 23.7% year-on-year in real terms in the first quarter of 2026, following an increase of 15.4% in the preceding quarter. The strong export growth was supported by the sustained global demand for AI-related electronic products and buoyant regional trade flows in Asia. Recent data still pointed to continued strengthening of export shipments within the region. Analysed by major market and with reference to external merchandise trade statistics, exports to the Mainland maintained double-digit growth. Exports to Association of Southeast Asian Nations markets continued to surge, and those to most advanced economies in Asia increased further. Exports to the United States showed strong growth, and those to the European Union grew solidly. On a seasonally adjusted quarter-to-quarter basis, total exports of goods rose notably by 15.9% in real terms in the first quarter.

Exports of services continued to expand solidly by 3.5% in real terms in the first quarter over a year earlier, after rising by 4.7% in the preceding quarter. Broad-based growth was seen across all major service groups. Specifically, exports of travel services continued to grow visibly, driven by strong inbound tourism. Exports of transport services and financial services grew moderately, amid solid performance in cross-boundary traffic and financial service activities. Exports of business and other services also showed moderate growth. On a seasonally adjusted quarter-to-quarter basis, exports of services decreased slightly by 0.4% in real terms in the first quarter.

Domestic sector

Private consumption saw accelerated growth in the first quarter of 2026, indicating a more entrenched recovery in households' spending. Private consumption expenditure rose by 4.9% in real terms in the first quarter over a year earlier, after an increase of 2.5% in the preceding quarter. On a seasonally adjusted quarter-to-quarter basis, private consumption expenditure rose by 1.7% in real terms. Meanwhile, government consumption expenditure increased by 3.0% in real terms in the first quarter over a year earlier, after rising by 1.5% in the preceding quarter. On a seasonally adjusted quarter-to-quarter basis, government consumption expenditure increased by 1.5% in real terms.

Overall investment expenditure in terms of gross domestic fixed capital formation continued to expand at a double-digit rate of 17.7% year-on-year in real terms in the first quarter, following an 11.7% increase in the preceding quarter. Expenditure on acquisitions of machinery, equipment and intellectual property products surged, with private sector spending showing particularly strong growth. Costs of ownership transfer soared amid active property transactions. Expenditure on building and construction turned to an increase, driven by a pick-up in the public sector.

Labour sector

The labour market showed modest improvement in the first quarter of 2026. The seasonally adjusted unemployment rate edged down further by 0.1 percentage point from the preceding quarter to 3.7% in the first quarter. The underemployment rate also decreased by 0.1 percentage point to 1.6%. The average monthly employment earnings of full-time employees (excluding foreign domestic helpers) continued to increase, by 5.6% in nominal terms or 4.0% in real terms in the first quarter over a year earlier.

Asset markets

The local stock market saw varying monthly performance during the first quarter of 2026. The HSI rallied to a four-and-a-half-year high of nearly 28 000 in January, moved sideways in February, and corrected in March after the Middle East conflict. The HSI closed the first quarter at 24 788, down by 3.3% from end-2025. Nevertheless, trading and fundraising activities remained strong throughout the quarter. More lately, since entering the second quarter, the HSI has largely recovered the earlier lost ground and returned to the pre-conflict levels. On May 13, the HSI closed at 26 388, up somewhat by 3.0% over end-2025.

The residential property market continued to strengthen in the first quarter. The number of transactions, in terms of the total number of sale and purchase agreements for residential property received by the Land Registry, increased notably further by 9% over the preceding quarter to 18 654 in the first quarter. This was the highest level since the third quarter of 2021, and also 53% higher than the level a year ago. Overall flat prices rose further by 4% during the first quarter. The index of home purchase affordability went up in the first quarter amid the continued rise in flat prices. Overall flat rentals rose further by 1% in the first quarter. The non-residential property market remained soft in the first quarter. Transactions of office space moderated, though those for retail shop space and flatted factories rose.

Prices

Consumer price inflation stayed modest in the first quarter of 2026, though it picked up somewhat in March, mainly driven by fuel-related components amid higher international oil prices. Price pressures in other components were largely contained. The underlying Composite CPI rose by 1.4% in the first quarter over a year earlier, following the 1.1% increase in the preceding quarter. Including the effects of the Government's one-off relief measures, the headline Composite CPI increased by 1.6% year-on-year in the first quarter.

Latest GDP and price forecasts for 2026

Looking ahead, Hong Kong's economic outlook remains broadly resilient. Strong global demand for advanced electronics and AIrelated products is expected to support goods export performance, while services exports should remain firm, underpinned by sustained vibrancy in inbound tourism, robust cross-boundary financial activity, and steady demand for business services. Relatively solid consumer sentiment and resilient business outlook are expected to support domestic demand. The impacts of the Middle East conflict on the Hong Kong economy have so far been limited. Yet, the outlook of the conflict remains highly uncertain. A further escalation or persistence of tensions could heighten global financial market volatility, posing downside risks to growth and upside risks to inflation.

Taking into account the stronger-than-expected outturn in the first quarter and the potential near-term headwinds in the external environment, the real GDP growth forecast for 2026 as a whole is maintained at 2.5% – 3.5%, the same as that announced in the Budget (Table 2). Risk to growth is tilted to the downside due to the uncertainty surrounding the actual outcome of the scale and duration of the Middle East conflict.

On the inflation outlook, the feed-through of higher international oil prices to fuel-related components in consumer prices should continue in the coming months. Overall inflation in Hong Kong is, however, expected to remain relatively well anchored, reflecting the city's low energy intensity as a predominantly service-oriented economy, with stable energy supplies from the Mainland helping to mitigate external shocks. Taking into account the actual inflation situation in the first quarter and the factors mentioned above, the forecasts for the underlying and headline consumer price inflation rates for 2026 are revised up to 2.5% and 2.6% respectively, from 1.7% and 1.8% as announced in the Budget (Table 2).

Source: HKSAR Government Press Releases

In the past two months, the Government has introduced short-term, targeted measures to provide timely relief to sectors with relatively high fuel cost. The Government remains vigilant to the risks of further escalation of the conflict, will closely monitor the developments, and will respond further as appropriate to safeguard price stability.

The First Quarter Economic Report 2026 is now available for online download, free of charge at www.hkeconomy.gov.hk/en/situation/index.htm. The Report of the Gross Domestic Product by Expenditure Component, which contains the GDP figures up to the first quarter of 2026, is also available for browse and download, free of charge on the homepage of the Census and Statistics Department, www.censtatd.gov.hk.

The Government Economist, Ms Irina Fan (centre), presents the First Quarter Economic Report 2026 at a press conference today (May 15). Also present are Principal Economist Mr Eric Lee (left) and Assistant Commissioner for Census and Statistics Ms Edith Chan (right). Source: HKSAR Government Press Releases