GUANGZHOU, China, Nov. 25, 2024 /PRNewswire/ -- GAC Group, one of China's largest automobile manufacturers, on November 15 released three groundbreaking models at the Guangzhou Auto Show 2024, spanning the electric, extended-range, and plug-in hybrid segments: the S7, AION UT, and HYPTEC HL.

The S7, a large five-seater SUV that GAC says is its first "advanced intelligence" vehicle, boasts a 2.6-meter light strip, third-gen PHEV system with 4WD and over 1,000 km of mixed range. It also features AI-driven ambient lighting with eight preset expressions for personalized mood-setting, taillights inspired by the Northern Lights, hidden door handles and rooftop LiDAR sensors, delivering a sleek, futuristic driving experience.

The AION UT, one of GAC's "global strategic model", also debuted at the show. Positioned as a top-tier battery electric vehicle, the UT is a smooth-silhouetted hatchback, standing out from its peers with its extra-long 2,750mm wheelbase, attractive oval-shaped headlights and minimalist C-shaped taillights.

This youthful design language is continued in the UT's interior, which features rounded corner details, a large floating central display and fully digital instrument panel. Another neat design innovation is the location of the charging port on the front fender, a small but effective change that demonstrates the extra attention to detail that the AION design team is famous for.

The Group's final debut model was the HYPTEC HL, a large six-seater which aims to redefine standards for luxury SUVs. 5,126mm in length, the HL is full of luxury features, including exquisite lighting displays, cut-above video and audio fittings, a suede rooftop and premium grade leather throughout, but what makes it stand out from competitors is a new focus on second row comfort. The HL features twin 18-point massage chairs for its second-row passengers, fitted with touchscreen displays, fast charging ports and extra-large armrests.

Under the hood, the HL is a powerhouse of new energy, with dual-power pure electric and extended range (EV+REV), 800V 5C super charging and non-sensing starting technology, and the world's first 30,000rpm amorphous electric drive. The car's pure electric range exceeds 350km, with a comprehensive range over 1200km.

These three new models highlight GAC Group's dedication to leading the smart electric vehicle market as part of the company's ongoing global expansion strategy. The era of electric travel is here, and China's electric-native brands are poised to share their ongoing breakthroughs in vehicle technology to the world.

** The press release content is from PR Newswire. Bastille Post is not involved in its creation. **

GAC Releases Three New Models at Guangzhou Auto Show: S7, AION UT, HYPTEC HL

|

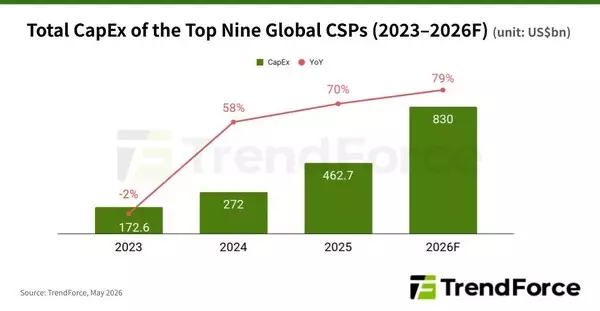

NEW YORK, May 6, 2026 /PRNewswire/ -- TrendForce's latest findings on the AI industry highlight that several major North American CSPs have recently raised their 2026 capital expenditure (CapEx) guidance in response to strong AI demand. As a result, TrendForce has revised its forecast for the combined CapEx of the world's top nine CSPs—Google, AWS, Meta, Microsoft, Oracle, ByteDance, Tencent, Alibaba, and Baidu—up to approximately US$830 billion in 2026, with the annual growth rate raised from 61% to 79%.

Taking a look at the four major U.S. CSPs, Microsoft has increased its CapEx outlook to $190 billion, implying approximately 130% YoY growth. Around roughly $25 billion is attributable to rising component costs. Similarly, Google has raised its guidance from $175–185 billion to $180–190 billion, with growth exceeding 100%. Meta has revised its CapEx range upward from $115–135 billion to $125–145 billion, representing approximately 85% YoY growth. Lastly, AWS is expected to exceed $230 billion in CapEx this year, with growth of over 50% driven by demand for AI cloud services.

TrendForce notes that the pace of CapEx expansion among North American CSPs exceeds the global average, underscoring that AI infrastructure has become a core long-term strategic priority. Investment is increasingly concentrated in the deployment of high-performance GPU clusters, in-house ASIC development, and next-generation data centers designed to support high-power-density computing.

The sharp rise in CapEx also signals sustained momentum in data center construction, led primarily by AWS, Microsoft, Google, Meta, and Oracle. As of the end of 2025, these five North American CSPs had deployed 800–900 data centers globally, with AWS accounting for the lion's share.

Among Chinese CSPs, Alibaba and ByteDance are the main drivers of expansion—though their strategies diverge. Alibaba is focusing on localized nodes and sovereign cloud offerings through Alibaba Cloud to penetrate emerging markets. Since announcing expansion plans in 2025, the company has established new regions in Brazil, France, and the Netherlands, enlarging its global footprint to 29 regions and 94 availability zones.

In contrast, ByteDance is aggressively expanding overseas through TikTok, with operations established across eight countries, including the U.S., Brazil, and Ireland, and major investments in Europe, Thailand, and Malaysia. This makes it the most geographically aggressive Chinese CSP.

TrendForce further notes that sustained AI demand will continue to drive global data center growth, with total installed power capacity expected to reach approximately 155 GW in 2026 (~+29% YoY). AI servers are also projected to surpass general-purpose servers in total electricity consumption in 2026 due to significantly higher power consumption per unit.

Further jumps in power consumption are expected in 2027–2028 as platforms such as GB300/Rubin and ASIC-based AI servers enter mass production. This trend will, in turn, support growth in key components such as HVDC power systems and liquid cooling systems.

For more information on TrendForce's semiconductor reports and market data, please visit the Report Page, or Email (SR_MI@trendforce.com) the Sales Department.

For more on the latest technology industry news and trends, please visit News.

About TrendForce

TrendForce is a global leader in technology industry analysis and consulting services. With deep expertise spanning foundry, DRAM, HBM, NAND Flash, AI servers, robotics, near-eye displays, display panels, LEDs, MLCC, and green energy, it also offers in-depth research into key market drivers such as AI, automotive technologies, 5G/6G communications, LEO satellites, and the IoT.

Backed by a team of top industry professionals, TrendForce has been at the forefront of global market research for over 25 years. More than 60% of its clients are among the world's top 500 companies.

TrendForce's global footprint includes Taipei, Shenzhen, Silicon Valley, New York, and Tokyo. With timely and strategic industry analysis, TrendForce delivers the critical information that empowers businesses to make smarter, faster decisions.

CONTACT: pengchen@trendforce.com

NEW YORK, May 6, 2026 /PRNewswire/ -- TrendForce's latest findings on the AI industry highlight that several major North American CSPs have recently raised their 2026 capital expenditure (CapEx) guidance in response to strong AI demand. As a result, TrendForce has revised its forecast for the combined CapEx of the world's top nine CSPs—Google, AWS, Meta, Microsoft, Oracle, ByteDance, Tencent, Alibaba, and Baidu—up to approximately US$830 billion in 2026, with the annual growth rate raised from 61% to 79%.

Taking a look at the four major U.S. CSPs, Microsoft has increased its CapEx outlook to $190 billion, implying approximately 130% YoY growth. Around roughly $25 billion is attributable to rising component costs. Similarly, Google has raised its guidance from $175–185 billion to $180–190 billion, with growth exceeding 100%. Meta has revised its CapEx range upward from $115–135 billion to $125–145 billion, representing approximately 85% YoY growth. Lastly, AWS is expected to exceed $230 billion in CapEx this year, with growth of over 50% driven by demand for AI cloud services.

TrendForce notes that the pace of CapEx expansion among North American CSPs exceeds the global average, underscoring that AI infrastructure has become a core long-term strategic priority. Investment is increasingly concentrated in the deployment of high-performance GPU clusters, in-house ASIC development, and next-generation data centers designed to support high-power-density computing.

The sharp rise in CapEx also signals sustained momentum in data center construction, led primarily by AWS, Microsoft, Google, Meta, and Oracle. As of the end of 2025, these five North American CSPs had deployed 800–900 data centers globally, with AWS accounting for the lion's share.

Among Chinese CSPs, Alibaba and ByteDance are the main drivers of expansion—though their strategies diverge. Alibaba is focusing on localized nodes and sovereign cloud offerings through Alibaba Cloud to penetrate emerging markets. Since announcing expansion plans in 2025, the company has established new regions in Brazil, France, and the Netherlands, enlarging its global footprint to 29 regions and 94 availability zones.

In contrast, ByteDance is aggressively expanding overseas through TikTok, with operations established across eight countries, including the U.S., Brazil, and Ireland, and major investments in Europe, Thailand, and Malaysia. This makes it the most geographically aggressive Chinese CSP.

TrendForce further notes that sustained AI demand will continue to drive global data center growth, with total installed power capacity expected to reach approximately 155 GW in 2026 (~+29% YoY). AI servers are also projected to surpass general-purpose servers in total electricity consumption in 2026 due to significantly higher power consumption per unit.

Further jumps in power consumption are expected in 2027–2028 as platforms such as GB300/Rubin and ASIC-based AI servers enter mass production. This trend will, in turn, support growth in key components such as HVDC power systems and liquid cooling systems.

For more information on TrendForce's semiconductor reports and market data, please visit the Report Page, or Email (SR_MI@trendforce.com) the Sales Department.

For more on the latest technology industry news and trends, please visit News.

About TrendForce

TrendForce is a global leader in technology industry analysis and consulting services. With deep expertise spanning foundry, DRAM, HBM, NAND Flash, AI servers, robotics, near-eye displays, display panels, LEDs, MLCC, and green energy, it also offers in-depth research into key market drivers such as AI, automotive technologies, 5G/6G communications, LEO satellites, and the IoT.

Backed by a team of top industry professionals, TrendForce has been at the forefront of global market research for over 25 years. More than 60% of its clients are among the world's top 500 companies.

TrendForce's global footprint includes Taipei, Shenzhen, Silicon Valley, New York, and Tokyo. With timely and strategic industry analysis, TrendForce delivers the critical information that empowers businesses to make smarter, faster decisions.

CONTACT: pengchen@trendforce.com

** This press release is distributed by PR Newswire through automated distribution system, for which the client assumes full responsibility. **

North American AI Data Center Expansion Drives 2026 CapEx of Top Nine CSPs to US$830 Billion, Says TrendForce