MUNICH, Feb. 19, 2025 /PRNewswire/ -- On February 17, 2025, GCL System Integration (GCL SI) achieved a significant milestone by securing the EcoVadis Group-level Silver Medal certification. In its first attempt, GCL SI stood out among over 150,000 participating companies globally, placing it within the top 15% of sustainable development leaders. This recognition marks GCL SI's advancement to world-class standards in Environmental, Social, and Governance (ESG) practices, setting a benchmark for sustainable development in the global renewable energy sector.

EcoVadis, a leading global CSR assessment organization that operates across 175 countries and over 200 industries, evaluates companies based on four key dimensions: environmental management, labor rights, business ethics, and sustainable procurement. GCL SI's Silver Medal achievement signifies that its ESG performance surpassed 85% of global participants, showcasing leadership in areas such as environmental governance and green supply chain management. Notably, GCL SI's proprietary carbon platform, "GCL Carbon Data Platform," integrates blockchain and privacy computing technology to track and manage the carbon emissions across the entire photovoltaic industry, promoting a circular green ecosystem.

In its efforts to advance green manufacturing, GCL SI has implemented a "Triple-Integration" strategy, combining digital empowerment with low-carbon technology upgrades, resulting in an annual reduction of 127,000 tons of COâ‚‚ equivalent emissions. The company has also established an intelligent energy management system that boosts photovoltaic plant operational efficiency by 23%.

As one of the global top five photovoltaic module suppliers, GCL SI remains commitment to its mission of "bringing green power to life". The company has built a green procurement system spanning 28 countries and 186 suppliers, resulting in an annual carbon reduction of 450,000 tons. Additionally, GCL SI has invested CNY 380 million to upgrade its intelligent manufacturing systems, and its Suzhou base was nominated as a "Lighthouse Factory" by the World Economic Forum.

Standing at the crossroads of the global energy transition, GCL SI continues to deepen its "Zero Carbon Technology + Digital Energy" dual-engine strategy, aiming for full carbon neutrality across its entire value chain by 2027. As the UN Global Compact's Asia-Pacific Executive Director stated: "GCL SI's ESG practices are redefining the global responsibility paradigm for renewable energy companies."

** The press release content is from PR Newswire. Bastille Post is not involved in its creation. **

GCL SI Achieves EcoVadis Silver Medal Certification, Ranks in the Global Top 15% for ESG Practices

|

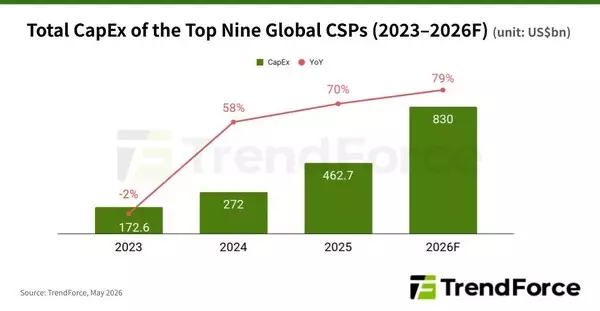

NEW YORK, May 6, 2026 /PRNewswire/ -- TrendForce's latest findings on the AI industry highlight that several major North American CSPs have recently raised their 2026 capital expenditure (CapEx) guidance in response to strong AI demand. As a result, TrendForce has revised its forecast for the combined CapEx of the world's top nine CSPs—Google, AWS, Meta, Microsoft, Oracle, ByteDance, Tencent, Alibaba, and Baidu—up to approximately US$830 billion in 2026, with the annual growth rate raised from 61% to 79%.

Taking a look at the four major U.S. CSPs, Microsoft has increased its CapEx outlook to $190 billion, implying approximately 130% YoY growth. Around roughly $25 billion is attributable to rising component costs. Similarly, Google has raised its guidance from $175–185 billion to $180–190 billion, with growth exceeding 100%. Meta has revised its CapEx range upward from $115–135 billion to $125–145 billion, representing approximately 85% YoY growth. Lastly, AWS is expected to exceed $230 billion in CapEx this year, with growth of over 50% driven by demand for AI cloud services.

TrendForce notes that the pace of CapEx expansion among North American CSPs exceeds the global average, underscoring that AI infrastructure has become a core long-term strategic priority. Investment is increasingly concentrated in the deployment of high-performance GPU clusters, in-house ASIC development, and next-generation data centers designed to support high-power-density computing.

The sharp rise in CapEx also signals sustained momentum in data center construction, led primarily by AWS, Microsoft, Google, Meta, and Oracle. As of the end of 2025, these five North American CSPs had deployed 800–900 data centers globally, with AWS accounting for the lion's share.

Among Chinese CSPs, Alibaba and ByteDance are the main drivers of expansion—though their strategies diverge. Alibaba is focusing on localized nodes and sovereign cloud offerings through Alibaba Cloud to penetrate emerging markets. Since announcing expansion plans in 2025, the company has established new regions in Brazil, France, and the Netherlands, enlarging its global footprint to 29 regions and 94 availability zones.

In contrast, ByteDance is aggressively expanding overseas through TikTok, with operations established across eight countries, including the U.S., Brazil, and Ireland, and major investments in Europe, Thailand, and Malaysia. This makes it the most geographically aggressive Chinese CSP.

TrendForce further notes that sustained AI demand will continue to drive global data center growth, with total installed power capacity expected to reach approximately 155 GW in 2026 (~+29% YoY). AI servers are also projected to surpass general-purpose servers in total electricity consumption in 2026 due to significantly higher power consumption per unit.

Further jumps in power consumption are expected in 2027–2028 as platforms such as GB300/Rubin and ASIC-based AI servers enter mass production. This trend will, in turn, support growth in key components such as HVDC power systems and liquid cooling systems.

For more information on TrendForce's semiconductor reports and market data, please visit the Report Page, or Email (SR_MI@trendforce.com) the Sales Department.

For more on the latest technology industry news and trends, please visit News.

About TrendForce

TrendForce is a global leader in technology industry analysis and consulting services. With deep expertise spanning foundry, DRAM, HBM, NAND Flash, AI servers, robotics, near-eye displays, display panels, LEDs, MLCC, and green energy, it also offers in-depth research into key market drivers such as AI, automotive technologies, 5G/6G communications, LEO satellites, and the IoT.

Backed by a team of top industry professionals, TrendForce has been at the forefront of global market research for over 25 years. More than 60% of its clients are among the world's top 500 companies.

TrendForce's global footprint includes Taipei, Shenzhen, Silicon Valley, New York, and Tokyo. With timely and strategic industry analysis, TrendForce delivers the critical information that empowers businesses to make smarter, faster decisions.

CONTACT: pengchen@trendforce.com

NEW YORK, May 6, 2026 /PRNewswire/ -- TrendForce's latest findings on the AI industry highlight that several major North American CSPs have recently raised their 2026 capital expenditure (CapEx) guidance in response to strong AI demand. As a result, TrendForce has revised its forecast for the combined CapEx of the world's top nine CSPs—Google, AWS, Meta, Microsoft, Oracle, ByteDance, Tencent, Alibaba, and Baidu—up to approximately US$830 billion in 2026, with the annual growth rate raised from 61% to 79%.

Taking a look at the four major U.S. CSPs, Microsoft has increased its CapEx outlook to $190 billion, implying approximately 130% YoY growth. Around roughly $25 billion is attributable to rising component costs. Similarly, Google has raised its guidance from $175–185 billion to $180–190 billion, with growth exceeding 100%. Meta has revised its CapEx range upward from $115–135 billion to $125–145 billion, representing approximately 85% YoY growth. Lastly, AWS is expected to exceed $230 billion in CapEx this year, with growth of over 50% driven by demand for AI cloud services.

TrendForce notes that the pace of CapEx expansion among North American CSPs exceeds the global average, underscoring that AI infrastructure has become a core long-term strategic priority. Investment is increasingly concentrated in the deployment of high-performance GPU clusters, in-house ASIC development, and next-generation data centers designed to support high-power-density computing.

The sharp rise in CapEx also signals sustained momentum in data center construction, led primarily by AWS, Microsoft, Google, Meta, and Oracle. As of the end of 2025, these five North American CSPs had deployed 800–900 data centers globally, with AWS accounting for the lion's share.

Among Chinese CSPs, Alibaba and ByteDance are the main drivers of expansion—though their strategies diverge. Alibaba is focusing on localized nodes and sovereign cloud offerings through Alibaba Cloud to penetrate emerging markets. Since announcing expansion plans in 2025, the company has established new regions in Brazil, France, and the Netherlands, enlarging its global footprint to 29 regions and 94 availability zones.

In contrast, ByteDance is aggressively expanding overseas through TikTok, with operations established across eight countries, including the U.S., Brazil, and Ireland, and major investments in Europe, Thailand, and Malaysia. This makes it the most geographically aggressive Chinese CSP.

TrendForce further notes that sustained AI demand will continue to drive global data center growth, with total installed power capacity expected to reach approximately 155 GW in 2026 (~+29% YoY). AI servers are also projected to surpass general-purpose servers in total electricity consumption in 2026 due to significantly higher power consumption per unit.

Further jumps in power consumption are expected in 2027–2028 as platforms such as GB300/Rubin and ASIC-based AI servers enter mass production. This trend will, in turn, support growth in key components such as HVDC power systems and liquid cooling systems.

For more information on TrendForce's semiconductor reports and market data, please visit the Report Page, or Email (SR_MI@trendforce.com) the Sales Department.

For more on the latest technology industry news and trends, please visit News.

About TrendForce

TrendForce is a global leader in technology industry analysis and consulting services. With deep expertise spanning foundry, DRAM, HBM, NAND Flash, AI servers, robotics, near-eye displays, display panels, LEDs, MLCC, and green energy, it also offers in-depth research into key market drivers such as AI, automotive technologies, 5G/6G communications, LEO satellites, and the IoT.

Backed by a team of top industry professionals, TrendForce has been at the forefront of global market research for over 25 years. More than 60% of its clients are among the world's top 500 companies.

TrendForce's global footprint includes Taipei, Shenzhen, Silicon Valley, New York, and Tokyo. With timely and strategic industry analysis, TrendForce delivers the critical information that empowers businesses to make smarter, faster decisions.

CONTACT: pengchen@trendforce.com

** This press release is distributed by PR Newswire through automated distribution system, for which the client assumes full responsibility. **

North American AI Data Center Expansion Drives 2026 CapEx of Top Nine CSPs to US$830 Billion, Says TrendForce