BOSTON--(BUSINESS WIRE)--Jul 30, 2025--

Fidelity Investments® today shared its 24 th annual Retiree Health Care Cost Estimate, revealing that a 65-year-old retiring in 2025 can expect to spend an average of $172,500 in health care and medical expenses throughout retirement 1. This represents a more than 4% increase over 2024 and continues the general upward trajectory of projected health-related expenses since Fidelity’s inaugural $80,000 estimate in 2002.

This press release features multimedia. View the full release here: https://www.businesswire.com/news/home/20250730447812/en/

This year’s estimate comes as Americans’ confidence in their retirement prospects has slightly decreased and a record-number begin their final stretch to reaching the traditional retirement age of 65 2. Of concern, recent Fidelity research shows 1-in-5 Americans say they have never considered health care needs during retirement—a figure that rises to one-in-four among Gen X. More so, across all generations, 17% have taken no action at all when it comes to planning for health expenses in retirement 3.

“Year after year, so many Americans underestimate how much they’ll need to save to cover health care costs in retirement,” said Shams Talib, head of Fidelity Workplace Consulting. “We recognize the impact health care costs can have on retirement savings. With the right tools and guidance, pre-retirees and retirees alike can take greater control of their financial futures by beginning the planning process as soon as possible.”

The Retiree Health Care Cost Estimate helps Americans of all ages understand the potential impact of rising health care costs on their financial planning and helps them make more informed decisions about saving for retirement. The estimate assumes enrollment in Original Medicare (Parts A and B) and Medicare Part D, which includes premiums, co-payments, and other out-of-pocket costs for medical care and prescription drugs. It does not include long-term care expenses.

Health Savings Accounts: a tax-advantaged tool for health care costs

Health savings accounts (HSAs) can play an important role in preparing for health care costs both now and in the future. The most notable feature of an HSA is its triple-tax advantage 4: contributions to the account are made pre-tax; you can withdraw funds to pay for qualified medical expenses tax-free; and you can invest HSA funds, too, with any investment growth also considered tax-free.

“HSAs are more than just a short-term savings tool—they can serve as a critical component of the retirement readiness equation,” said Steve Betts, head of Fidelity Health. “Our research consistently shows HSA users feel more prepared to cover health care expenses in retirement, yet many people don’t realize the full potential of the account. When used as a part of a well-crafted retirement plan, the tax-advantaged nature of your HSA savings can offer growth potential that can help reduce the burden of health care in retirement.”

While HSA adoption rates continue to increase— Fidelity HSAs saw a 43% growth in total assets and 23% increase in accounts in 2024 5 —opportunities still exist for greater education around HSA features. Recent Fidelity research finds only 23% of Americans say they are contributing to an HSA as one way to prepare for health care costs in retirement, and just 3-in-10 are investing their HSA assets, leaving growth potential on the table 3. Moreover, many pre-retirees have fallen into an HSA knowledge gap altogether: only 15% of people ages 55-64 have an HSA 6, and among them, more than half (52%) are not aware that an HSA can be used as a retirement savings vehicle 7.

Medicare: the difference a plan makes

For older Americans approaching Medicare eligibility, understanding the potential costs they may face in retirement is critical, as well as how Medicare can and cannot help. While 37% of Americans plan to rely on Medicare to cover health care costs in retirement 2, Fidelity’s estimate—which assumes enrollment in Medicare Parts A. B, and D—shows how quickly out-of-pocket expenses can add up. Retirees are still on the hook to cover things like Medicare premiums, over-the-counter medications, dental and vision care, and other types of added expenses like long-term care.

Choosing health care coverage in retirement can be one of the most complex decisions many Americans make—55% anticipate it will be difficult to enroll in Medicare coverage, and half expect to be confused when selecting a plan. 8 Whether enrolling in Medicare for the first time or looking for coverage to better meet their needs, Fidelity Medicare Services ® can help by providing complimentary education and guidance from licensed insurance agents to help retirees and near-retirees with their health and financial goals.

Fidelity Resources for Managing Your Health Care Journey Today and Into Retirement

About Fidelity Investments

Fidelity’s mission is to strengthen the financial well-being of our customers and deliver better outcomes for the clients and businesses we serve. Fidelity’s strength comes from the scale of our diversified, market-leading financial services businesses that serve individuals, families, employers, wealth management firms, and institutions. With assets under administration of $15.0 trillion, including discretionary assets of $5.9 trillion as of March 31, 2025, we focus on meeting the unique needs of a broad and growing customer base. Privately held for 78 years, Fidelity employs more than 77,000 associates across the United States, Ireland, and India. For more information about Fidelity Investments, visit https://www.fidelity.com/about-fidelity/our-company.

###

Investing involves risk, including risk of loss.

The information provided here is general in nature. It is not intended, nor should it be construed, as legal or tax advice. Because the administration of an HSA is a taxpayer responsibility, customers are strongly encouraged to consult their tax advisor before opening an HSA. Customers are also encouraged to review information available from the Internal Revenue Service (IRS) for taxpayers, which can be found on the IRS Web site at www.IRS.gov. They can find IRS Publication 969, Health Savings Accounts and Other Tax-Favored Health Plans, and IRS Publication 502, Medical and Dental Expenses (including the Health Coverage Tax Credit), online, or you can call the IRS to request a copy of each at 800.829.3676.

Fidelity does not provide legal or tax advice. The information herein is general in nature and should not be considered legal or tax advice. Consult an attorney or tax professional regarding your specific situation.

Views expressed are as of the date indicated, based on the information available at that time, and may change based on market or other conditions. Unless otherwise noted, the opinions provided are those of the speaker or author and not necessarily those of Fidelity Investments or its affiliates. Fidelity does not assume any duty to update any of the information.

Fidelity Medicare Services® is operated by Fidelity Health Insurance Services, LLC (“FHIS”), and FMR LLC (“FMR”) is the parent company of FHIS. Unless otherwise indicated, the information and items published in this document are provided by FHIS for informational purposes only and are not intended as tax, legal, or investment advice.

We do not offer every plan available in your area. Please contactwww.medicare.govor 1-800-MEDICARE (TTY users should call 1-877-486-2048), 24 hours a day/7 days a week or your local State Health Insurance Program (SHIP) to get information on all of your options.

Fidelity Medicare Services (“FMS”) and Fidelity Brokerage Services LLC (“FBS”) are separate business entities. FMS is not a product or service of FBS. Other than certain demographic information such as name, address and date of birth, the information you provide to FMS or FBS will not be shared with the other entity. Therefore, if you want FBS to consider the information you have provided to FMS in your investment planning with FBS, you must separately provide that information to FBS.

The services described are provided by FHIS. In this capacity, FHIS acts as an insurance broker or agent (collectively referred to as a “Producer”). FHIS and its representatives are appropriately licensed in all states in which they conduct business.

FHIS and its producers are certified representatives of insurance carriers that provide Medicare Supplement insurance as well as are certified representatives of Medicare Advantage (HMO, PPO and PFFS) organizations (and stand-alone prescription drug plans) with a Medicare contract.

The insurance products are issued by third-party insurance companies, which are unaffiliated with FHIS and FMR.

FHIS earns a commission paid by the insurance company based on your enrollment in a health plan. FHIS agents and representatives are not compensated based on your enrollment in a health plan and do not receive commissions from third-party insurance companies.

ATTENTION: Medicare has neither reviewed nor endorsed the information in this document/website. Fidelity Medicare Services, FHIS, and FMR are not connected with or endorsed by the U.S. government or the Centers for Medicare & Medicaid Services.

For a complete list of available plans, please contact 1-800-MEDICARE (TTY users should call 1-877-486-2048) 24 hours a day/7 days a week or consult www.medicare.gov.

This may be considered an advertisement or solicitation for insurance.

Fidelity Health Insurance Services, Corporate Trust Center, 1209 Orange Street, Wilmington, DE 19801

Fidelity Brokerage Services LLC, Member NYSE, SIPC,

900 Salem Street, Smithfield, RI 02917

Fidelity Distributors Company LLC,

900 Salem Street, Smithfield, RI 02917

National Financial Services LLC, Member NYSE, SIPC,

245 Summer Street, Boston, MA 02205

1213876.1.0

© 2025 FMR LLC. All rights reserved

1 Estimate based on a single person retiring in 2025, 65-years-old, with life expectancies that align with Society of Actuaries' RP-2014 Healthy Annuitant rates projected with Mortality Improvements Scale MP-2020 as of 2022. Actual assets needed may be more or less depending on actual health status, area of residence, and longevity. Estimate is net of taxes. The Fidelity Retiree Health Care Cost Estimate assumes individuals do not have employer-provided retiree health care coverage, but do qualify for the federal government’s insurance program, original Medicare. The calculation takes into account Medicare Part B base premiums and cost-sharing provisions (such as deductibles and coinsurance) associated with Medicare Part A and Part B (inpatient and outpatient medical insurance). It also considers Medicare Part D (prescription drug coverage) premiums and out-of-pocket costs, as well as certain services excluded by original Medicare. The estimate does not include other health-related expenses, such as over-the-counter medications, most dental services and long-term care.

2 Social Security Administration Historical and Projected Population Estimates 1940-2100 (2023)

3 Fidelity Investments 2025 State of Retirement Planning Study

4 With respect to federal taxation only. Contributions, investment earnings, and distributions may or may not be subject to state taxation.

5 Devenir Research 2024 Year-End HSA Market Statistics & Trends

6 “2022 Devenir & HSA Council Demographic Survey,” Devenir Research, July 13, 2023, https://www.devenir.com/wp-content/uploads/2022-Devenir-and-HSA-Council-Demographic-Report.pdf

7 Fidelity Health Thought Leadership Benefit Plan Participant Survey, fall 2023, Q14: “[That Health Savings Accounts (HSAs) can be used as an investment and retirement savings vehicle] Overall, how aware are you of each of the below?” Sample included 688 consumers ages 55 or older without an HAS

8 This CARAVAN study presents the findings of a survey among a sample of 2,009 U.S. adults ages 50+. Interviewing was conducted on June 27-July 2, 2024 by Big Village, which is not affiliated with Fidelity Investments. The results may not be representative of all adults meeting the same criteria as those surveyed.

9 Morningstar rated 10-11 retail HSA providers for HSAs as a spending account to cover current medical costs and HSAs as an investment account to save for future medical expenses. Results published in 2019, 2020, 2021, 2022, 2023, and 2024 “Health Savings Account Landscape.”

10 Devenir Research 2024 Year-End HSA Market Statistics and Trends

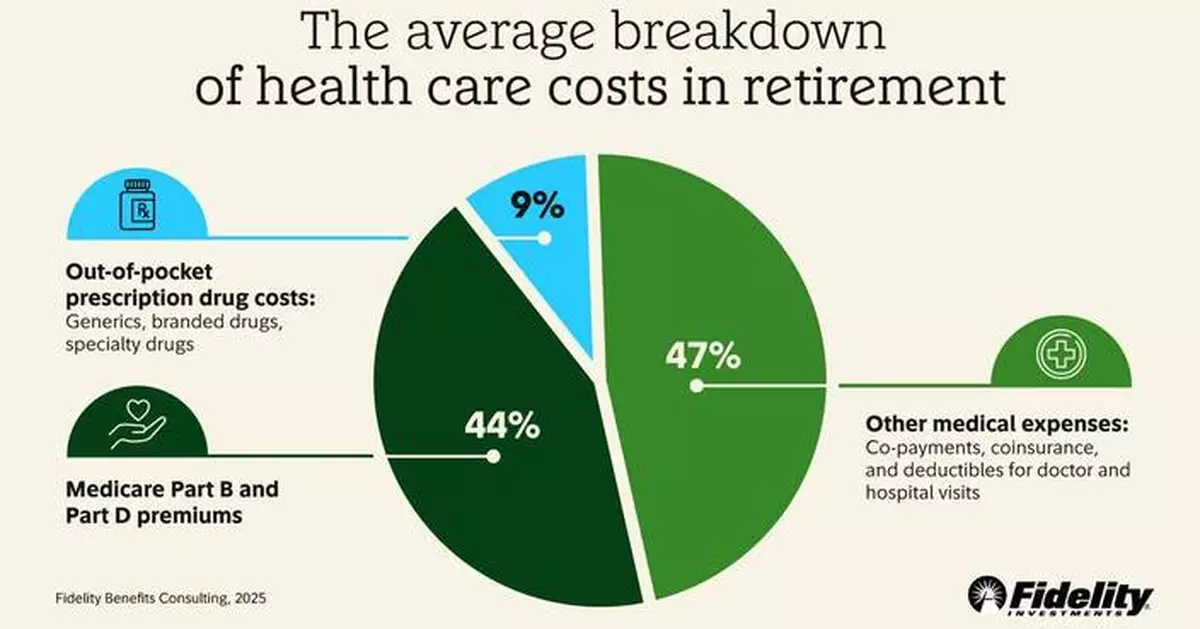

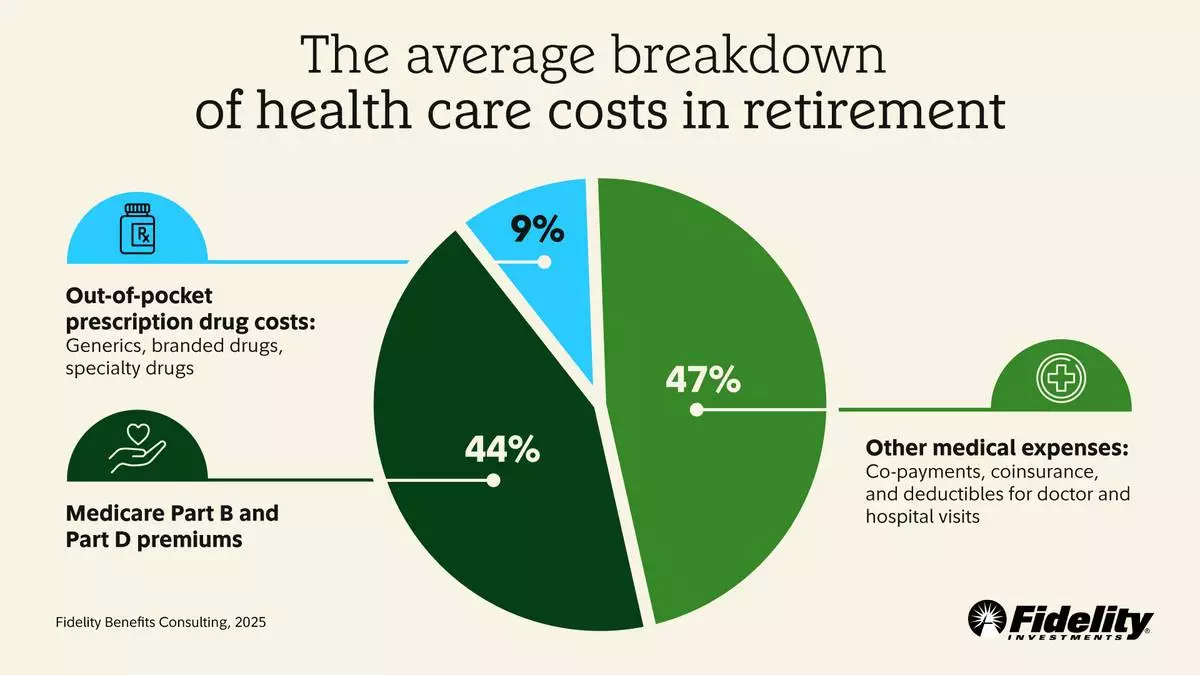

How Fidelity's estimate of $172,500 breaks down, on average