CASA GRANDE, Ariz. & TORONTO--(BUSINESS WIRE)--Sep 2, 2025--

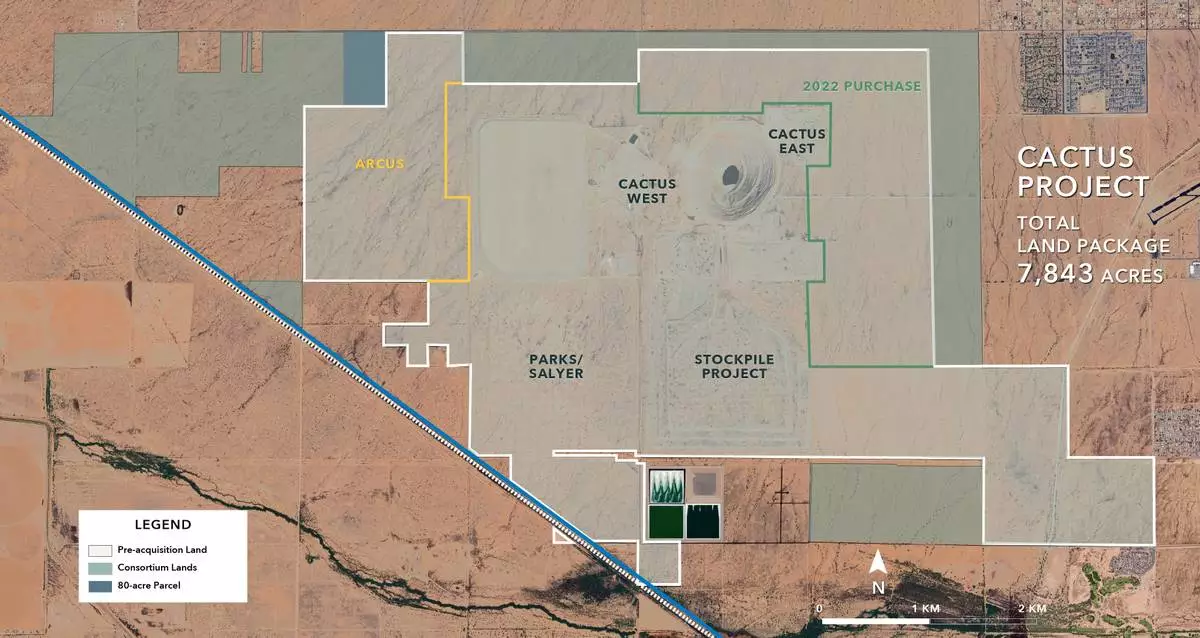

Arizona Sonoran Copper Company Inc. (TSX:ASCU | OTCQX:ASCUF) (“ ASCU ” or the “ Company ”), an emerging US-based copper developer, acquired 2,123 acres of private land adjacent to the Cactus Project (see FIGURE 1 ), comprised of 2,043 acres from a consortium of related private corporate landowners (collectively, the “ Consortium Land ”) and completed on August 29, 2025, plus an additional 80-acre parcel (the “ 80-acre Parcel ”) acquired from a single private corporate landowner on June 27, 2025. The Consortium Land together with the 80-acre Parcel (collectively, the “ Purchased Lands ”) are expected to provide the additional acreage necessary to support the anticipated development and operations plan for the Cactus Project, including the solvent extraction/electrowinning (“ SX/EW ”) plant infrastructure, leach pads and waste rock stockpiles (collectively, the “ ProjectPlan ”). All dollar amounts are in U.S. currency unless specified otherwise.

This press release features multimedia. View the full release here: https://www.businesswire.com/news/home/20250902584056/en/

Highlights:

See below for a detailed summary of principal transaction terms for the Purchased Lands.

George Ogilvie, ASCU President and CEO, “During the ongoing advancement of the pending Pre-Feasibility Study, it became evident that while the necessary water and mineral rights were in place, once the estimated mine life extended past year 15, additional acreage for eventual surface operations would be needed. We foresaw this potential and contemplated the acquisition of approximately 2,000 acres of additional private land within the 2024 Preliminary Economic Assessment. With the addition of the Purchased Lands, contiguous to the Cactus Project and of corresponding scale, we believe that all land requirements are now in place to support the anticipated Project Plan, including a significant heap-leach and SX/EW copper cathode operation. The acquisition of this land package consequently represents a major de-risking event for the Cactus Project, as well as providing additional real estate to potentially pursue development of the primary sulphide deposits and future exploration opportunities, within the previously held project properties. Additionally, the favorable structure, cost of capital, pre-payment rights and other principal terms of these land purchases, provide a financially manageable path forward for the Company and the Cactus Project through the remaining studies to project financing and an eventual final investment decision as early as Q4/2026. With the completion of these acquisitions, the overall average cost-per-acre of the Cactus Project private land package now stands at approximately $23,000, quite favourable considering the extent of the contiguous acreage of private lands acquired adjacent to the developing Casa Grande industrial area, and which includes the Parks/Salyer and Cactus deposits. This well-timed execution of the opportunity to purchase a contiguous 2,123-acre land package from known, local private property owners, is clearly a positive step forward for the Cactus Project. We welcome the Consortium Vendors as new supportive shareholders of the Company and as key stakeholders in the Cactus Project.”

PURCHASED LANDS

Consortium Land

On August 29, 2025, Cactus 110 LLC, an ASCU wholly-owned subsidiary (“ Cactus 110 ”), signed and closed a real estate purchase and sale agreement with a consortium of related private corporate land owners (collectively, the “ Consortium Vendors ”) pursuant to which Cactus 110 purchased 2,043 acres (the “ Consortium Transaction ”). The Consortium Land includes 100% of the surface rights to such lands as well as all mineral rights held by the Consortium Vendors, representing approximately 80% of the underlying mineral title. The purchase price for the Consortium Land was $50,000 per acre (the “Consortium Purchase Price ”), with $5 million paid on the closing ($2 million in cash and 1,549,487 common shares at a deemed price of C$2.66 per share, representing $3 million value equivalent) and the balance deferred subject to applicable Vendor Loans at an interest rate of six percent (6%) per annum accruing and capitalized annually, and payable on maturity in 2029, per the following schedule, with Cactus 110 having the right to pre-pay such loans, in whole or in part, at any time, without penalty:

The Company anticipates having project financing for the Cactus Project in place as early as Q4/2026, a portion of which could be used to pre-pay the Consortium Vendors Loans, in full, in advance of maturity on August 29, 2029.

The number of ASCU common shares issued in each instance under the Consortium Transaction, in lieu of cash at Cactus 110’s sole option, will be determined using a 5-day volume weighted average trading price of ASCU common shares on the TSX immediately preceding the applicable payment due date, subject to customary TSX and other applicable regulatory approvals, and a statutory hold period under applicable securities laws. ASCU welcomes the Consortium Vendors as new shareholders of the Company and key stakeholders in the Cactus Project.

Each of the Consortium Vendor Loans are secured by deed of trust on their respectively sold portions of the Consortium Land (and fixtures thereon) and a deed of trust on the ~750 acre ARCUS lands already owned by Cactus 110. In addition, one of the Consortium Vendors will hold additional security for its Vendor Loan pursuant to a modified deed of trust on 1,000 acres purchased by Cactus 110 in 2022 (see FIGURE 1 ) from that Consortium Vendor (the“ 2022 Seller ”), which remains subject to a final deferred purchase price payment of $5 million due, interest-free, by February 10, 2027 (the “ 2022 Property Loan ”). The Consortium Vendor Loans are subject to cross-default with one another, and the 2022 Property Loan is subject to cross-default with the Vendor Loan from the 2022 Seller. Payment defaults under the Consortium Vendor Loans are subject to favourable cure periods of 30 days on the 2026, 2027, and 2028 payments and 90 days on the final payment due in 2029. A default on the final 2027 payment due under the 2022 Property Loan is subject to a favourable cure period of 60 days.

In addition to the Consortium Purchase Price, an aggregate 0.5% net smelter returns royalty (“ NSR ”) on the Consortium Land was granted to a designee of the Consortium Vendors, on terms consistent with other NSRs on the Cactus Project. Cactus 110 has a right of first refusal on any sale, transfer, assignment or other conveyance of the NSR by the Consortium Vendors’ designee, other than to an affiliate.

Upon any transfer or sale, whether voluntarily or involuntarily, directly or indirectly, of greater than fifty percent (50%) in Cactus 110 or the Cactus Project, prior to payment in full of the amounts due and owing under the Consortium Vendor Loans, such transferee(s)/purchaser(s) shall be required to acknowledge and affirm, in writing, the binding nature of the continuing applicable terms of the Consortium Transaction and the Consortium Vendor Loans.

The Consortium Transaction and related Vendor Loans are otherwise generally subject to customary terms and conditions for real estate transactions in Arizona.

80-acre Parcel

On June 27, 2025, Cactus 110 completed the purchase of the 80-acre Parcel, including 100% of the surface and underlying mineral rights, pursuant to a real estate purchase and sale agreement with a private corporate landowner (the “ 80-acre Vendor ”) dated and effective as of April 29, 2025 (the “ 80-acre Purchase ”). The 80-acre Purchase price was $30,000 per acre, with $1.2 million paid in cash on closing, with the remaining $1.2 million deferred subject to a non-interest-bearing Vendor Loan, to be paid in full in cash by maturity on June 27, 2026, with Cactus 110 having the right to pre-pay such loan, in whole or in part, at any time, without penalty. The 80-acre Vendor Loan is secured by deed of trust on the 80-acre Parcel (see FIGURE 1 ), under which Cactus 110 has up to 90 days to cure any payment or other default under the Vendor Loan. The 80-acre Purchase and related Vendor Loan is otherwise subject to customary terms and conditions for real estate transactions in Arizona.

Link from the press release:

FIGURE 1 (Map): https://arizonasonoran.com/projects/cactus-mine-project/press-release-images/

Neither the TSX nor the regulating authority has approved or disproved the information contained in this press release.

About Arizona Sonoran Copper Company (www.arizonasonoran.com|www.cactusmine.com)

ASCU is a copper exploration and development company with a 100% interest in the brownfield Cactus Project. The Project, on privately held land, contains a large-scale porphyry copper resource and a recent 2024 PEA proposes a generational open pit copper mine with robust economic returns. Cactus is a lower risk copper developer benefitting from a State-led permitting process, in place infrastructure, highways and rail lines at its doorstep and onsite permitted water access. The Company objective is to develop Cactus and become a mid-tier copper producer with low operating costs, that could generate robust returns and provide a long-term sustainable and responsible operation for the community, investors and all stakeholders. The Company is led by an executive management team and Board which have a long-standing track record of successful project delivery in North America complemented by global capital markets expertise.

Cautionary Statements regarding Forward-Looking Statements and Other Matters

Forward-Looking Statements

All statements, other than statements of historical fact, contained or incorporated by reference in this press release constitute “forward-looking statements” and “forward-looking information” (collectively, “forward-looking statements”) within the meaning of applicable Canadian and United States securities legislation. Generally, these forward-looking statements can be identified by the use of forward-looking terminology such as “advance”, “anticipated”, “assumptions”, “become”, “believe”, “could”, “delivery”, “de-risking”, “developer”, “development”, “emerging”, “estimated”, “eventual”, “expected”, “exploration”, “feasibility”, “flexibility”, “following”, “forward”, “future”, “generational”, “indicated”, “initial”, “intention”, “long-term”, “manageable”, “objective”, “opportunity”, “option”, “path”, “pending”, “plan”, “potentially”, “predict”, “preliminary”, “program”, “projected”, “proposes”, “pursue”, “required”, “rights”, “risk”, “study”, “subject to”, “will”, and “would”, or variations of such words, and similar such words, expressions or statements that certain actions, events or results can, could, may, should, would, will (or not) be achieved, occur, provide, result or support in the future, or which, by their nature, refer to future events. In some cases, forward-looking information may be stated in the present tense, such as in respect of current matters that may be continuing, or that may have a future impact or effect. Forward-looking statements include those relating to the payment of the Vendor Loans (including the allocation of cash and ASCU shares to make payments under the Consortium Vendor Loans, the related TSX and other required approvals, and any corresponding issuances of ASCU shares, accrual and corresponding payment of interest) and the satisfaction or enforcement of such and other terms of the Vendor Loans (including any pre-payment, re-payment, defaults or cure thereof, enforcement of security under the applicable deeds of trust or otherwise or recourse under the deeds of trust and enforcement thereof) and timing and implications of any thereof; payment of the 2022 Property Loan and the satisfaction or enforcement of such and other terms thereof; the benefits and other implications of the acquisition of the Purchased Lands (including that such lands will provide the additional land, acreage or real estate necessary to support, or the resulting consolidated land package will meet supporting land requirements for, the anticipated development and operations plan for the Cactus Project including the solvent extraction/electrowinning (or SX/EW) plant infrastructure, leach pads and waste rock stockpiles (or the Project Plan), or sufficient to meet the land requirements thereof or necessary to support potential development of any incremental mineralization identified by future exploration and/or existing primary sulphide mineralization at the Cactus Project (including any corresponding or resulting operational flexibility to do so) and any such pursuit and results thereof); future exploration (including identification of any incremental mineralization and any development thereof); any development of the primary sulphide mineralization; the pending PreFeasibility Study (or PFS) and other ongoing and future technical studies (including any definitive feasibility study) and the continuation, completion, execution, results and/or implications of such studies, and timing thereof; the Project Plan (including completion, land requirements and other details thereof); mine life or life of mine; project financing (including advancement thereof, getting such in place and available, terms and the timing thereof, and ability and/or decision to use the proceeds of any such financing to pre-pay the Vendor Loans); any final investment decision (including the outcome or execution, and timing thereof); the de-risking of the Cactus Project; the results of the 2024 PEA (including capital intensity, production, mine life (or life of mine), returns and other economics; and the Company’s objectives (including development of the Cactus Project, becoming a mid-tier copper producer with low operating costs, that could generate robust returns and provide a long-term sustainable and responsible operation for the community, investors and all stakeholders, and any other continuing or future successes). Although the Company believes that such statements are reasonable, there can be no assurance that those forward-looking statements will prove to be correct, and any forward-looking statements by the Company are not guarantees of future actions, results or performance. Forward-looking statements are based on assumptions, estimates, expectations and opinions, which are considered reasonable and represent best judgment based on available facts, as of the date such statements are made. If such assumptions, estimates, expectations and opinions prove to be incorrect, actual and future results may be materially different than expressed or implied in the forward-looking statements. The assumptions, estimates, expectations and opinions referenced, contained or incorporated by reference in this press release which may prove to be incorrect include those set forth or referenced in this press release, as well as those stated in the most recent technical report for the Cactus Project filed on August 27, 2024 (the “2024 PEA Technical Report”), the Company’s Annual Information Form dated March 27, 2025 (the “AIF”), Management’s Discussion and Analysis (together with the accompanying financial statements) for the year ended December 31, 2024 and the quarters already ended in 2025 (collectively, the “2024-25 Financial Disclosure”) and the Company’s other applicable public disclosure (collectively, “Company Disclosure”), all available on the Company’s website at www.arizonasonoran.com and under its issuer profile at www.sedarplus.ca. Forward-looking statements are inherently subject to known and unknown risks, uncertainties, contingencies and other factors which may cause the actual results, performance or achievements of ASCU to be materially different from any future results, performance or achievements expressed or implied by the forward-looking statements. Such risks, uncertainties, contingencies and other factors include default under, and related enforcement of, the Vendor Loans and/or the 2022 Property Loan (including foreclosure and other remedies under the related security or applicable law); the Purchased Lands not providing sufficient additional land, acreage or real estate necessary to support the Project Plan, or being insufficient to meet the land requirements thereof or to potentially pursue development of the existing primary sulphide deposit and/or future exploration opportunities (including not providing any corresponding or resulting operational flexibility to do so) or at all and, in any event, that such pursuit thereof does not occur, in whole or in part and, if so, that the results do not meet expectations; future exploration not identifying any incremental mineralization or, if identified, development thereof not being economic and/or otherwise not meeting expectations, or otherwise not occurring at all; the existing primary sulphide mineralization not being economic and/or not being developed for other reasons or not otherwise not meeting expectations; defects in, contest over or other challenges to, or competing interests in surface and/or mineral title to, other interests in, or intended use of the Purchased Lands and other properties comprising the Cactus Project; the Company not securing project financing for the Cactus Project on the anticipated or an otherwise acceptable timeline, or on acceptable terms, or at all, and the consequences thereof (including inability to make payments under the Vendor Loans, on time or at all, and on making and the outcome of any final investment decision and timing thereof, if any decision at all); the inability to make the remaining payment under the 2022 Property Loan; the pending Pre-Feasibility Study and other ongoing and future technical studies (including any definitive feasibility study) not being consistent with the Company’s expectations (including the completion, execution, results and/or implications of such studies, and timing thereof; the results of the 2024 Preliminary Economic Assessment (or 2024 PEA) differing from the pending Pre-Feasibility Study (including, among other things, capital intensity, production, mine life (or life of mine), returns and other economics); and the accuracy of the current mineral resource estimates (or MRE) for the Cactus Project and the Company’s analysis thereof not being consistent with expectations (including but not limited to ore tonnage and ore grade estimates), and future MRE for the Cactus Project not being consistent with the current MRE or plans and/or models for the Cactus Project (see also further cautionary statements below under the heading “ Mineral Resource Estimates ”), among other risks, uncertainties, contingencies and other factors, including the “Risk Factors” in the AIF, and the risks, uncertainties, contingencies and other factors identified in the 2024 PEA Technical Report and the 2024-25 Financial Disclosure. The foregoing list of risks, uncertainties, contingencies and other factors is not exhaustive; readers should consult the more complete discussion of the Company’s business, financial condition and prospects that is provided in the AIF, the 2024-25 Financial Disclosure and other Company Disclosure. Although ASCU has attempted to identify important factors that could cause actual actions, events or results to differ materially from those described in forward-looking statements, there may be other factors that cause actions, events or results to differ from those anticipated, estimated or intended. Forward-looking statements contained herein are made as of the date of this press release (or as otherwise expressly specified) and ASCU disclaims any intention or obligation to update or revise any forward-looking statements, whether as a result of new information, future events or results or otherwise, except as required by applicable securities laws. There can be no assurance that such information will prove to be accurate, as actual results and future events could differ materially from forward-looking statements. Accordingly, readers should not place undue reliance on forward-looking statements. The forward-looking statements referenced or contained in this press release are expressly qualified by these Cautionary Statements as well as the Cautionary Statements in the AIF, the 2024 PEA Technical Report, the 2024-25 Financial Disclosure and other Company Disclosure.

Preliminary Economic Assessments

The Preliminary Economic Assessment (or 2024 PEA) referenced in this press release and summarized in the 2024 PEA Technical Report is only a conceptual study of the potential viability of the Cactus Project and the economic and technical viability of the Cactus Project has not been demonstrated. The 2024 PEA is preliminary in nature and provides only an initial, high-level review of the Cactus Project’s potential and design options; there is no certainty that the 2024 PEA will be realized. For further detail on the Cactus Project and the 2024 PEA, including applicable technical notes and cautionary statements, please refer to the Company’s press release dated August 7, 2024 and the 2024 PEA Technical Report, both available on the Company’s website at www.arizonasonoran.com and under its issuer profile at www.sedarplus.ca.

FIGURE 1 (September 2, 2025 PR) - ASCU acquired 2,123 acres of private land adjacent to the Cactus Project (see FIGURE 1), comprised of 2,043 acres from a consortium of related private corporate landowners (collectively, the “Consortium Land”) and completed on August 29, 2025, plus an additional 80-acre parcel (the “80-acre Parcel”) acquired from a single private corporate landowner on June 27, 2025. The Consortium Land together with the 80-acre Parcel (collectively, the “Purchased Lands”) are expected to provide the additional acreage necessary to support the anticipated development and operations plan for the Cactus Project, including the solvent extraction/electrowinning (“SX/EW”) plant infrastructure, leach pads and waste rock stockpiles (collectively, the “Project Plan”).