HONG KONG SAR - Media OutReach Newswire - 10 November 2025 - CPA Australia's regional survey about business technology adoption shows that most companies in Hong Kong have used artificial intelligence (AI) tools at different levels. Though the increasing AI application helps to improve productivity, it also transforms the hiring trends in the accounting and finance industry, and increases concerns on data protection and governance, according to the survey findings.

CPA Australia Survey: Increasing AI Adoption Reshapes Future Roles in Accounting Industry and Rises Data Concerns in Hong Kong

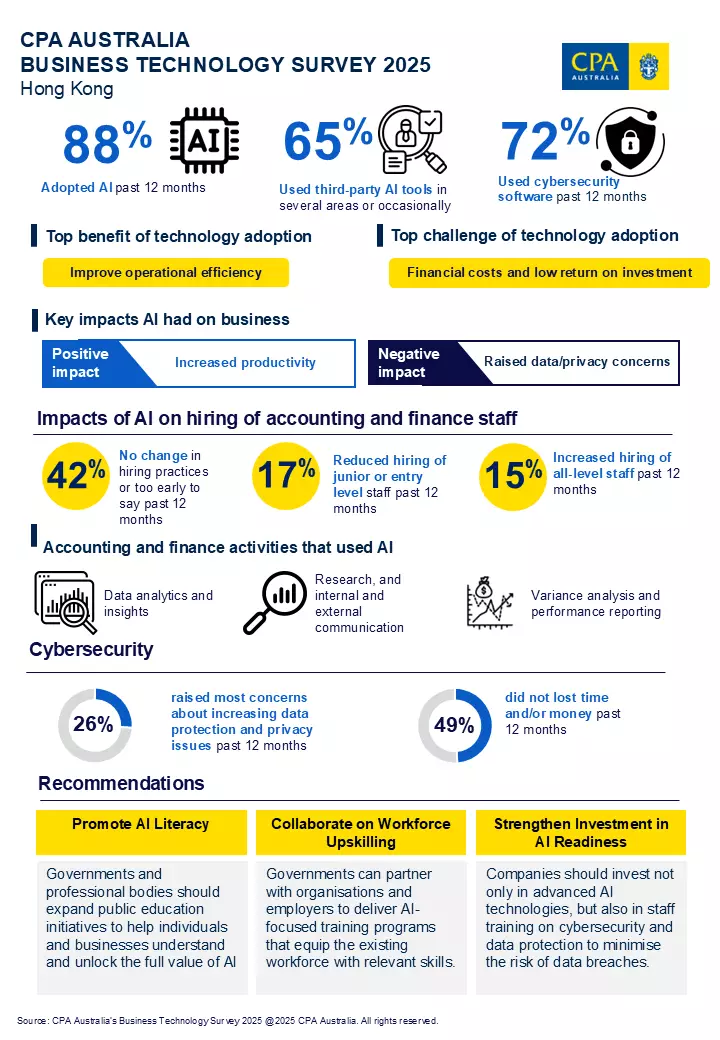

The result indicates the notable growth of AI adoption across markets in Asia Pacific, with 89 per cent of respondents said that they have adopted AI in the past 12 months, up from 69 per cent last survey. In Hong Kong, 88 per cent have applied AI such as ChatGPT, Copilot at the workplace. When asked about the level of AI adoption, 65 per cent respondents primarily used third-party tools in several areas or occasionally.

Dr Paul Sin, CPA Australia's Greater China Councillor and Chair of Web3 & Emerging Technology Committee highlighted the gap between the awareness of AI and releasing the real value of AI, "Most respondents said that they used third-party AI tools, implying that the awareness of AI in Hong Kong is high. Yet, many companies are still at the Proof-of-Concept stage, which means they just use AI tools to improve productivity like handling repetitive tasks and automate process. In fact, the government and professional organisations can do more education to unleash the true value of AI, for example, to reinvent business models or transform workflows by using more advanced solutions like predictive analytics and agentic AI, eventually scale up to production-grade implementation to align with their strategic goals."

The increasing prevalence of AI is transforming the recruitment trends across various industries including accounting and finance. While 42 per cent of respondents in Hong Kong said that there has been no change in hiring practices, or that is too early to say, 17 per cent said that their organisations have reduced the number of junior-level staff hired for the accounting and finance teams due to the adoption of AI.

Dr Sin highlighted the correlation between the hiring trend and the tasks being replaced by AI, "Survey shows that most respondents use AI for data analytics and research in their accounting and finance activities, and these tasks are usually carried out by junior staff. Clearly, AI can free them up from repetitive and tedious tasks, allowing them focus on more human-centric or strategic responsibilities such as advisory, decision-making and client engagement. The underlying skills are difficult to replace with technology such as creativity and judgement built from business experience. Grooming junior staff to take on these more advanced responsibilities takes time, so employers should consider balancing adoption of advanced technology with talent development for the organisation's long-term growth."

Dr Albert Wong, Deputy Chair of CPA Australia's Greater Bay Area Committee added on, "AI is only replacing certain tasks, not humans. As AI develops, the recruitment standard for technical skills is rising because some tasks can be done effectively by technology. Employers will expect their future staff to be able to work alongside with AI to solve problems, use these technology solutions to add value to existing services and products, generate new ideas/options, and predict the future in various scenarios. The job market will become more competitive. Therefore, the younger generation and the existing employees must develop irreplaceable skills, particularly soft skills such as human-human and human-machine interaction, effective communication, creative and critical thinking, and professional scepticism."

To keep up with the transformation, the Hong Kong SAR Government has an instrumental role to play. He called for policy support to build a future-ready workforce in Hong Kong. "The Government could collaborate with organisations and employers to upskill existing workforce on AI-centric training; offer subsidies to encourage SMEs to pilot/adopt different types of AI in their businesses and create internship schemes that give university students the opportunity to apply AI tools to real-world problem-solving."

Data is the new oil for technology. Among the surveyed markets, Hong Kong respondents raised the most concerns about increasing data protection and privacy issues (26 per cent) from AI adoption. On a positive note, 72 per cent said that they had implemented cybersecurity in the past 12 months, and Hong Kong's overall cybersecurity maturity is considerably high.

Mr Winson Woo, a member of CPA Australia's Greater Bay Area Committee shared his views on data protection and governance, "Many technologies already have embedded AI functions, so AI adoption will continue to increase in the future. Organisations should establish an AI development roadmap to plan how to apply AI to achieve strategic goals, and how to measure the return of investment, as well as setting clear governance guidelines to ensure the ethical use of AI tools in the workplace."

When discussing cybersecurity, he highlighted two emerging trends: Manage Security Operations Center (MSOC), a model of outsourcing security operations center (SOC) functions to third-party service providers to perform real-time detection and monitoring of cyber attacks and threats; and AI security, which protects AI systems from data breaches and misuse. He also emphasised the importance of staff training in data protection, "To reduce the risk of data leakage, companies should invest not only in technical software, but also in enhancing staff's security awareness, to ensure that AI users understand which authorised data can be used in AI tools and which sensitive information cannot be disclosed."

Mr Woo believes that the introduction of guidelines and regulations, such as the Personal Data (Privacy) Ordinance and the Protection of Critical Infrastructure (Computer System) Ordinance, will help to create an ethical environment that promotes innovation and technology in Hong Kong.

The survey collected responses from 1,117 accounting and finance professionals across markets in the Asia-Pacific such as Australia, mainland China, including 154 responses from Hong Kong.

Hashtag: #CPAAustralia

The issuer is solely responsible for the content of this announcement.

About CPA Australia

CPA Australia is one of the largest professional accounting bodies in the world, with nearly 175,000 members in over 100 countries and regions, including more than 22,500 members in Greater China. CPA Australia is celebrating its 70th anniversary in Hong Kong this year. Our core services include education, training, technical support and advocacy. CPA Australia provides thought leadership on issues affecting the accounting profession and the public interest. We engage with governments, regulators and industries to advocate policies that stimulate sustainable economic growth and have positive business and public outcomes. Find out more at cpaaustralia.com.au

** The press release content is from Media OutReach Newswire. Bastille Post is not involved in its creation. **

Prudent Risk Management Yields Solid Outcomes metrics, Core Pawn Business Demonstrates Resilient Growth with Proposed Final Dividend of HK$1.15 cents per share

Results Highlights:

- Profit for the year attributable to shareholders increased by approximately 47.8% YoY to approximately HK$82.6 million

- Net profit margin increased by approximately 16.2 p.p. YoY to approximately 50.2%

- Impairment losses recognized on loan receivables decreased by approximately 72.6% YoY to HK$12.7 million

- Revenue from pawn loan business increased by approximately 12.9% YoY to approximately HK$98.6 million

- Proposed final dividend of HK$1.15 cents per share

HONG KONG SAR - Media OutReach - 27 May 2026 - The board of directors of Oi Wah Pawnshop Credit Holdings Limited (HKEx stock code: 1319.HK, the "Group" or "Oi Wah") announced its annual results and its financial position. For the year ended 28 February 2026 ("FY2026"), the Group recorded revenue of approximately HK$164.4 million. Profit attributable to shareholders of the Company reached approximately HK$82.6 million, representing an increase of 47.8% compared to the year ended 28 February 2025 ("FY2025"). During the year, net interest margin expanded to approximately 17.2%.

As of 28 February 2026, the cash and cash equivalents (net of bank overdraft) amounted to approximately HK$376.9 million, representing a substantial increase of approximately 74.8% YoY. The net assets increased to approximately HK$1,155.7 million. Concurrently, the gearing ratio dropped to 4.1%. During the year, the earnings per share increased by approximately 48.3% YoY to HK 4.3 cents. The Board of Directors recommends a final dividend of HK 1.15 cents per share.

BUSINESS REVIEW

Mortgage loan business

In FY2026, the economy entered a phase of gradual recovery, leading to a steady resurgence in financing demand. The revenue from the mortgage loan business was approximately HK$65.8 million and accounted for approximately 40.0% of the Group's total revenue during the year. The gross mortgage loan receivables were approximately HK$612.5 million as at 28 February 2026. During the year, net interest margin of the mortgage loan business was approximately 10.1%.

In FY2026, the Group maintained a disciplined and risk-sensitive approach in its lending activities. While we observed an encouraging stabilization in the residential property market, the Group exercised intensified vigilance toward the commercial and industrial sectors due to persistent supply overhangs and valuation pressures. Our underwriting strategy remained focused on building a resilient loan portfolio by prioritizing high-quality collaterals and prudent loan-to-value ratios. During the year, the average loan-to-value ratio for first mortgage was approximately 56.27%, while overall average loan-to-value ratio for subordinate mortgage was approximately 40.82% of which, average loan-to-value ratio of subordinate mortgage that the Group participated in was approximately 3.73%.

Reflecting our robust credit risk management, the charge for impairment losses recognized on loan receivables decreased from approximately HK$46.3 million to approximately HK$12.7 million, representing a decrease of approximately 72.6% or HK$33.6 million.

Pawn Loan Business

The revenue from the pawn loan business increased by approximately 12.9% to approximately HK$98.6 million in FY2026. The business's profitability was further bolstered by a significant 73.0% increase in the gain on disposal of repossessed assets, which reached approximately HK$19.2 million as compared to approximately HK$11.1 million in FY2025. This performance was mainly attributed to the unprecedented strength of gold prices and a highly active secondary market for luxuries, particularly high-end timepieces. These factors have further solidified the pawn loan business as a resilient and strategic hedge against broader economic volatility.

During the year, the Group continued to channel resources to advertising and promotion to enhance the Group's brand exposure. Such effort has generated demand for one-to-one pawn loan appointment services for pawn loans exceeding HK$0.1 million.

PROSPECTS

Looking ahead, the Group maintains a stance of cautious optimism regarding the global economic recovery. While macroeconomic and geopolitical uncertainties may persist, we remain dedicated to a proactive yet prudent strategy to ensure sustainable long-term growth and maximize returns for our shareholders.

Within the mortgage loan market, our strategy will be characterized by a calibrated and divergent approach. We continue to hold an optimistic outlook on the residential property segment, where we intend to capitalize on the stabilizing interest rate environment by identifying high-quality mortgage opportunities. Conversely, we maintain cautious and vigilant towards the commercial and industrial sectors. Given the structural challenges of inventory overhang and the increasing prevalence of distressed assets, the Group will exercise intensified oversight in its credit underwriting and collateral appraisal to mitigate valuation risks.

Regarding our core operations, we anticipate our pawn loan business to remain resilient, supported by a firm gold price trajectory and sustained demand for liquidity management. To further enhance operational efficiency, the Group is actively optimizing its pawn shop network. We are strategically identifying more cost-effective locations within our established service areas, aiming to relocate our pawn outlets to premises with more competitive lease terms to reduce operating overheads while maintaining our leading market presence.

Simultaneously, our strategic partnership with PACM Group remains a key driver for geographic diversification. By proactively exploring institutional credit opportunities in developed markets while maintaining rigorous investment oversight, the Group is well-positioned to navigate evolving industry dynamics and deliver stable value to all stakeholders.

Mr. Edward Chan, Chairman and CEO of the Company, said, "Global geopolitical and macroeconomic uncertainties intertwine, placing pressure on the global economic recovery and posing ongoing challenges to the local property market. In the face of a complex external environment, Oi Wah has consistently adhered to a proactive yet prudent management strategy. Our core pawn loan business has fully demonstrated its role as a strategic tool to hedge against macroeconomic fluctuations, showcasing the Group's strong resilience amidst market challenges.

Looking forward, we will adopt a carefully calibrated differentiation strategy and continue to drive regional diversification. Under strict investment monitoring, we will actively explore business opportunities in developed markets to further expand our revenue streams and customer base, striving to deliver long-term, stable, and sustainable returns for our shareholders."

Hashtag: #OiWah

The issuer is solely responsible for the content of this announcement.

About Oi Wah Pawnshop Credit Holdings Limited

Oi Wah is a financing service provider in Hong Kong, mainly providing short-term secured financing, including pawn loans and mortgage loans. The Group established its first pawnshop in 1975 and currently owns 10 pawnshops and one premium service center in various locations in Hong Kong. Oi Wah diversified into mortgage loan business in 2009. The Group is the first local pawn shop which successfully listed on the Main Board of The Stock Exchange of Hong Kong Limited on 12 March 2013.

Results Highlights:

- Profit for the year attributable to shareholders increased by approximately 47.8% YoY to approximately HK$82.6 million

- Net profit margin increased by approximately 16.2 p.p. YoY to approximately 50.2%

- Impairment losses recognized on loan receivables decreased by approximately 72.6% YoY to HK$12.7 million

- Revenue from pawn loan business increased by approximately 12.9% YoY to approximately HK$98.6 million

- Proposed final dividend of HK$1.15 cents per share

HONG KONG SAR - Media OutReach - 27 May 2026 - The board of directors of Oi Wah Pawnshop Credit Holdings Limited (HKEx stock code: 1319.HK, the "Group" or "Oi Wah") announced its annual results and its financial position. For the year ended 28 February 2026 ("FY2026"), the Group recorded revenue of approximately HK$164.4 million. Profit attributable to shareholders of the Company reached approximately HK$82.6 million, representing an increase of 47.8% compared to the year ended 28 February 2025 ("FY2025"). During the year, net interest margin expanded to approximately 17.2%.

As of 28 February 2026, the cash and cash equivalents (net of bank overdraft) amounted to approximately HK$376.9 million, representing a substantial increase of approximately 74.8% YoY. The net assets increased to approximately HK$1,155.7 million. Concurrently, the gearing ratio dropped to 4.1%. During the year, the earnings per share increased by approximately 48.3% YoY to HK 4.3 cents. The Board of Directors recommends a final dividend of HK 1.15 cents per share.

BUSINESS REVIEW

Mortgage loan business

In FY2026, the economy entered a phase of gradual recovery, leading to a steady resurgence in financing demand. The revenue from the mortgage loan business was approximately HK$65.8 million and accounted for approximately 40.0% of the Group's total revenue during the year. The gross mortgage loan receivables were approximately HK$612.5 million as at 28 February 2026. During the year, net interest margin of the mortgage loan business was approximately 10.1%.

In FY2026, the Group maintained a disciplined and risk-sensitive approach in its lending activities. While we observed an encouraging stabilization in the residential property market, the Group exercised intensified vigilance toward the commercial and industrial sectors due to persistent supply overhangs and valuation pressures. Our underwriting strategy remained focused on building a resilient loan portfolio by prioritizing high-quality collaterals and prudent loan-to-value ratios. During the year, the average loan-to-value ratio for first mortgage was approximately 56.27%, while overall average loan-to-value ratio for subordinate mortgage was approximately 40.82% of which, average loan-to-value ratio of subordinate mortgage that the Group participated in was approximately 3.73%.

Reflecting our robust credit risk management, the charge for impairment losses recognized on loan receivables decreased from approximately HK$46.3 million to approximately HK$12.7 million, representing a decrease of approximately 72.6% or HK$33.6 million.

Pawn Loan Business

The revenue from the pawn loan business increased by approximately 12.9% to approximately HK$98.6 million in FY2026. The business's profitability was further bolstered by a significant 73.0% increase in the gain on disposal of repossessed assets, which reached approximately HK$19.2 million as compared to approximately HK$11.1 million in FY2025. This performance was mainly attributed to the unprecedented strength of gold prices and a highly active secondary market for luxuries, particularly high-end timepieces. These factors have further solidified the pawn loan business as a resilient and strategic hedge against broader economic volatility.

During the year, the Group continued to channel resources to advertising and promotion to enhance the Group's brand exposure. Such effort has generated demand for one-to-one pawn loan appointment services for pawn loans exceeding HK$0.1 million.

PROSPECTS

Looking ahead, the Group maintains a stance of cautious optimism regarding the global economic recovery. While macroeconomic and geopolitical uncertainties may persist, we remain dedicated to a proactive yet prudent strategy to ensure sustainable long-term growth and maximize returns for our shareholders.

Within the mortgage loan market, our strategy will be characterized by a calibrated and divergent approach. We continue to hold an optimistic outlook on the residential property segment, where we intend to capitalize on the stabilizing interest rate environment by identifying high-quality mortgage opportunities. Conversely, we maintain cautious and vigilant towards the commercial and industrial sectors. Given the structural challenges of inventory overhang and the increasing prevalence of distressed assets, the Group will exercise intensified oversight in its credit underwriting and collateral appraisal to mitigate valuation risks.

Regarding our core operations, we anticipate our pawn loan business to remain resilient, supported by a firm gold price trajectory and sustained demand for liquidity management. To further enhance operational efficiency, the Group is actively optimizing its pawn shop network. We are strategically identifying more cost-effective locations within our established service areas, aiming to relocate our pawn outlets to premises with more competitive lease terms to reduce operating overheads while maintaining our leading market presence.

Simultaneously, our strategic partnership with PACM Group remains a key driver for geographic diversification. By proactively exploring institutional credit opportunities in developed markets while maintaining rigorous investment oversight, the Group is well-positioned to navigate evolving industry dynamics and deliver stable value to all stakeholders.

Mr. Edward Chan, Chairman and CEO of the Company, said, "Global geopolitical and macroeconomic uncertainties intertwine, placing pressure on the global economic recovery and posing ongoing challenges to the local property market. In the face of a complex external environment, Oi Wah has consistently adhered to a proactive yet prudent management strategy. Our core pawn loan business has fully demonstrated its role as a strategic tool to hedge against macroeconomic fluctuations, showcasing the Group's strong resilience amidst market challenges.

Looking forward, we will adopt a carefully calibrated differentiation strategy and continue to drive regional diversification. Under strict investment monitoring, we will actively explore business opportunities in developed markets to further expand our revenue streams and customer base, striving to deliver long-term, stable, and sustainable returns for our shareholders."

Hashtag: #OiWah

The issuer is solely responsible for the content of this announcement.

About Oi Wah Pawnshop Credit Holdings Limited

Oi Wah is a financing service provider in Hong Kong, mainly providing short-term secured financing, including pawn loans and mortgage loans. The Group established its first pawnshop in 1975 and currently owns 10 pawnshops and one premium service center in various locations in Hong Kong. Oi Wah diversified into mortgage loan business in 2009. The Group is the first local pawn shop which successfully listed on the Main Board of The Stock Exchange of Hong Kong Limited on 12 March 2013.

** This press release is distributed by Media OutReach Newswire through automated distribution system, for which the client assumes full responsibility. **