NEW YORK (AP) — Oil prices are down, and stocks are up Monday, though such moves have been quick to reverse since the war in Iran began.

The S&P 500 jumped 1.2% and was on track for its best day in five weeks. The Dow Jones Industrial Average was up 513 points, or 1.1%, as of 10 a.m. Eastern time, and the Nasdaq composite was 1.3% higher.

Click to Gallery

Christopher Lagana works on the floor at the New York Stock Exchange in New York, Tuesday, March 10, 2026. (AP Photo/Seth Wenig)

Screens display financial information on the floor at the New York Stock Exchange in New York, Tuesday, March 10, 2026. (AP Photo/Seth Wenig)

Screens display financial information on the floor at the New York Stock Exchange in New York, Tuesday, March 10, 2026. (AP Photo/Seth Wenig)

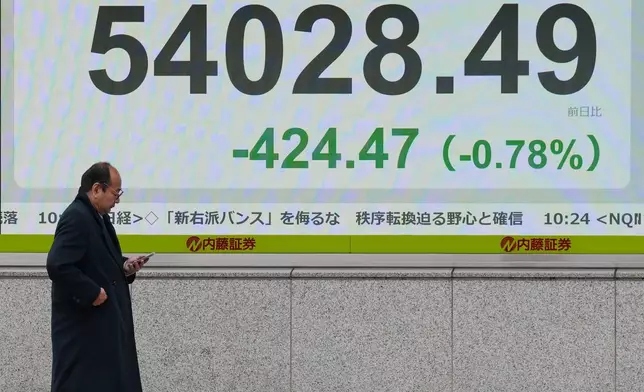

A person walks in front of an electronic stock board showing Japan's Nikkei index at a securities firm Friday, March 13, 2026, in Tokyo. (AP Photo/Eugene Hoshiko)

A person walks in front of an electronic stock board showing Japan's Nikkei index at a securities firm Friday, March 13, 2026, in Tokyo. (AP Photo/Eugene Hoshiko)

A person walks in front of an electronic stock board showing Japan's Nikkei index at a securities firm Friday, March 13, 2026, in Tokyo. (AP Photo/Eugene Hoshiko)

A person walks in front of an electronic stock board showing Japan's Nikkei index at a securities firm Friday, March 13, 2026, in Tokyo. (AP Photo/Eugene Hoshiko)

The driver for markets once again was the price of oil. A barrel of benchmark U.S. crude fell 5.3% to $93.57, easing some pressure off the economy after topping $102 earlier in the morning. Brent crude, the international standard, fell 2% to $101.09 per barrel after earlier getting as high as $106.50.

It's a reprieve, for now at least, after oil prices spiked from roughly $70 before the United States and Israel began their attacks on Iran. In response, Iran has effectively halted traffic through the narrow Strait of Hormuz, where a fifth of the world’s oil typically sails from the Persian Gulf to customers worldwide. That has oil producers cutting production because their crude has nowhere to go.

The worry in financial markets is that if the strait remains closed for a long time, it could keep enough oil off the market to drive inflation up to a debilitating level for the global economy.

President Donald Trump over the weekend demanded that other countries hurt by the closure of the Strait of Hormuz “take care of that passage” and said his country “will help - A LOT!”

European countries, meanwhile, demanded to know more about Trump’s plans for the war on Iran and when the conflict might end as they weighed his demand.

The U.S. stock market has a track record of bouncing back relatively quickly from military conflicts in the Middle East and elsewhere, as long as oil prices don’t stay too high for too long. Many professional investors are still expecting that to be the case again, which has helped keep U.S. stock prices near their record levels.

For all its dramatic swings, including several that struck hour to hour, the S&P 500 is still only about 4% below its all-time high.

Escalations have been mounting quickly, to be sure, but that could suggest “both sides are facing growing constraints that may prevent a long conflict,” according to Paul Christopher, head of global investment strategy at Wells Fargo Investment Institute.

On Wall Street, stocks of companies with big fuel bills helped lead the market thanks to falling oil prices. Norwegian Cruise Line Holdings steamed 4.2% higher, while United Airlines climbed 3.8% to trim their sharp losses for the year so far.

National Storage Affiliates leaped 28.5% after Public Storage said it would buy its 69 million rentable square feet in an all-stock deal valuing it at $10.5 billion. Public Storage fell 2.5%.

Dollar Tree rose 4.3% after reporting a stronger profit for the latest quarter than analysts expected, even as fewer shoppers visited its stores.

Nebius Group, a Dutch AI cloud company, saw its stock that trades in the United States leap 14% after announcing a five-year infrastructure contract with Meta Platforms that could be worth up to $27 billion. Meta rose 2.8% and was one of the strongest forces lifting the S&P 500, along with other Big Tech stocks.

In stock markets abroad, indexes rose in Europe, including a 1% return for Germany's DAX, following a mixed finish in Asia.

Stocks jumped 1.4% in Hong Kong but slipped 0.3% in Shanghai.

In the bond market, Treasury yields eased as falling oil prices took some pressure off inflation worries. A report showing a weakening of manufacturing activity in New York state also weighed on yields.

The yield on the 10-year Treasury fell to 4.22% from 4.28% late Friday.

Yields, though, are still higher than they were before the war, when the 10-year Treasury yield was at just 3.97%. Traders have pushed back their expectations for when the Federal Reserve could resume its cuts to interest rates because of the spike in oil prices caused by the war.

Such cuts would give the economy and job market a boost, and they're something Trump has angrily been calling for, but they would also worsen inflation. Traders see virtually no chance the Fed will announce a cut to rates when its next meeting concludes on Wednesday, according to data from CME Group.

AP Business Writers Matt Ott and Elaine Kurtenbach contributed.

Christopher Lagana works on the floor at the New York Stock Exchange in New York, Tuesday, March 10, 2026. (AP Photo/Seth Wenig)

Screens display financial information on the floor at the New York Stock Exchange in New York, Tuesday, March 10, 2026. (AP Photo/Seth Wenig)

Screens display financial information on the floor at the New York Stock Exchange in New York, Tuesday, March 10, 2026. (AP Photo/Seth Wenig)

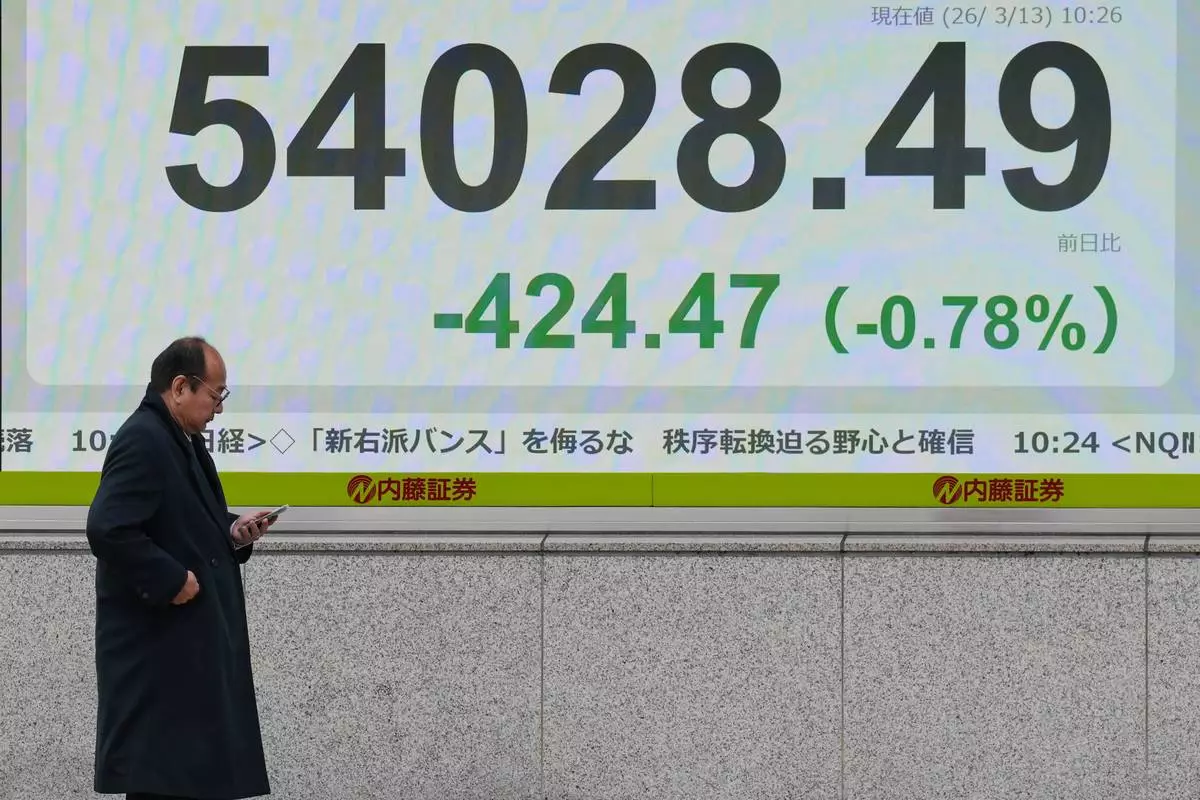

A person walks in front of an electronic stock board showing Japan's Nikkei index at a securities firm Friday, March 13, 2026, in Tokyo. (AP Photo/Eugene Hoshiko)

A person walks in front of an electronic stock board showing Japan's Nikkei index at a securities firm Friday, March 13, 2026, in Tokyo. (AP Photo/Eugene Hoshiko)

A person walks in front of an electronic stock board showing Japan's Nikkei index at a securities firm Friday, March 13, 2026, in Tokyo. (AP Photo/Eugene Hoshiko)

A person walks in front of an electronic stock board showing Japan's Nikkei index at a securities firm Friday, March 13, 2026, in Tokyo. (AP Photo/Eugene Hoshiko)