WALTHAM, Mass.--(BUSINESS WIRE)--Feb 10, 2026--

Pegasystems Inc. (NASDAQ: PEGA), the Enterprise Transformation Company™, released its financial results for the fourth quarter and full-year 2025.

This press release features multimedia. View the full release here: https://www.businesswire.com/news/home/20260210969541/en/

“2025 was an extraordinary year of progress and execution,” said Alan Trefler, founder and CEO, Pega. “We’re entering a transformative era with bold ideas and compelling innovation. Our approach positions us to lead the industry, deliver extraordinary value to clients, and enable clients to overcome legacy system limitations.”

“Our 2025 results reflect strong financial discipline, with top and bottom-line beats of our guidance and exceeding the Rule of 40,” Pega COO & CFO, Ken Stillwell, said. “Our recurring business model and our technology leadership position us to continue to accelerate ACV growth, expand margins, and increase free cash flow.”

Financial and performance metrics (1)

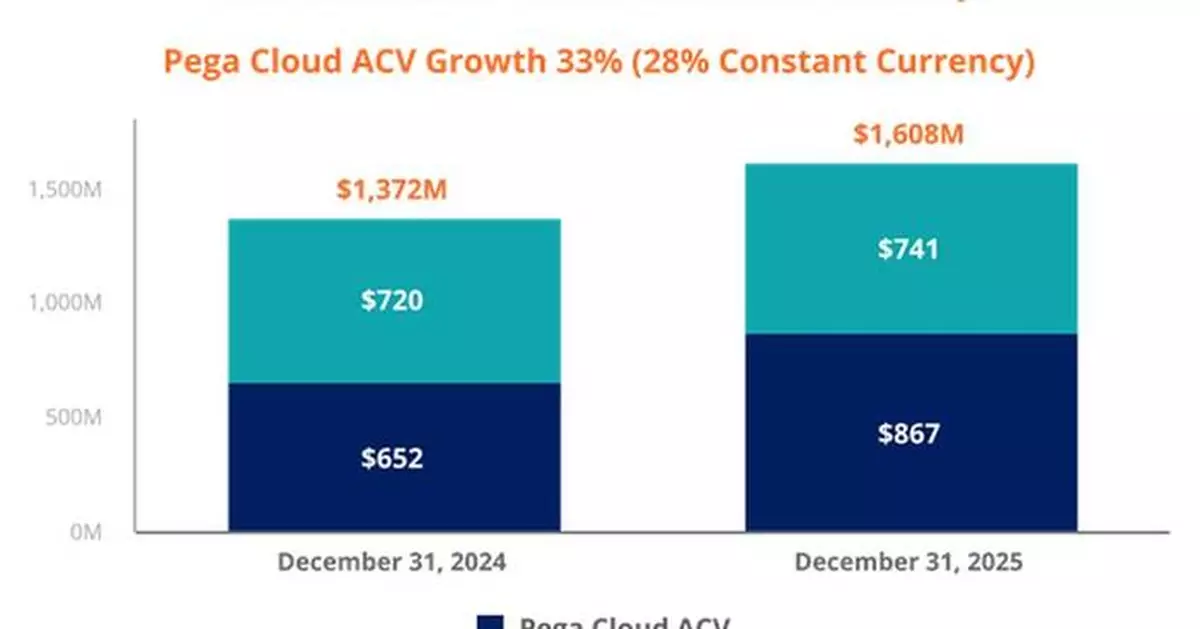

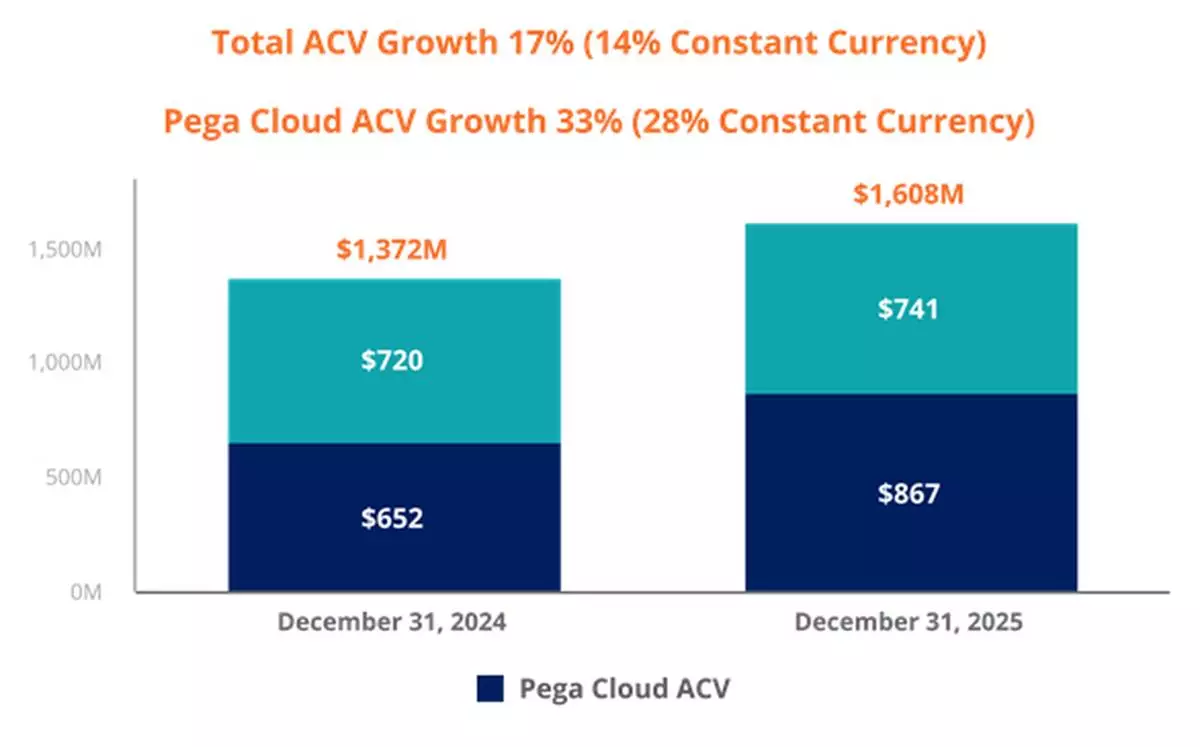

Reconciliation of ACV and Constant Currency ACV

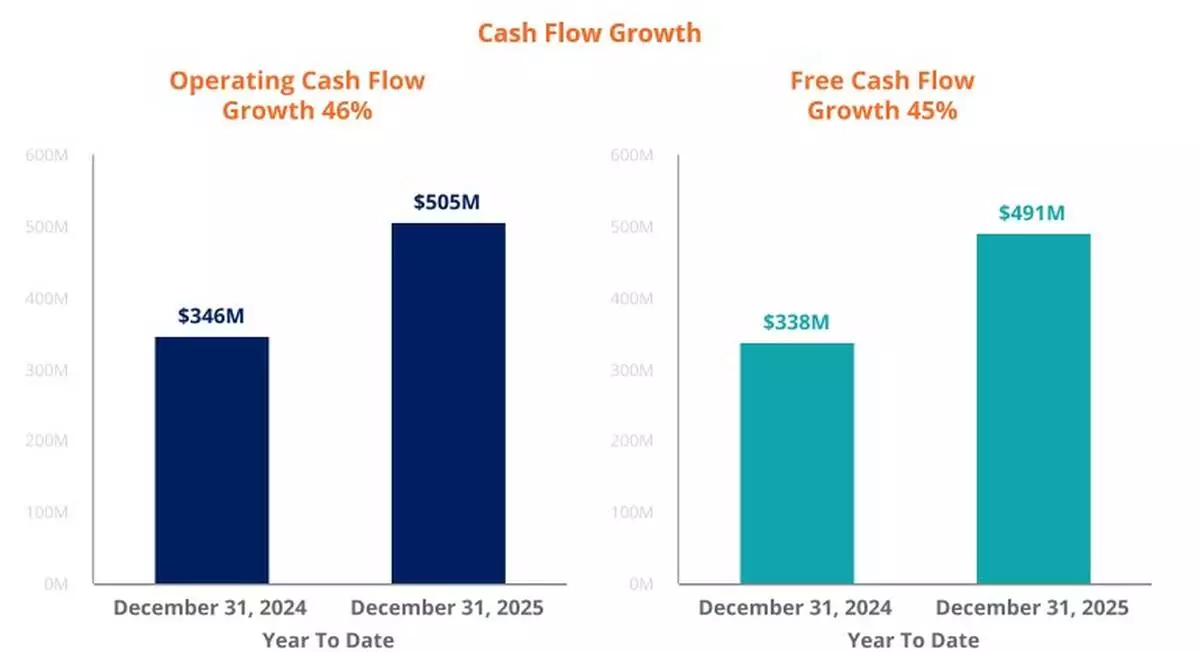

Cash Flow Growth

2026 Guidance (1)

As of February 10, 2026, we are providing the following guidance:

Quarterly conference call

A conference call and audio-only webcast will be conducted at 8:00 a.m. EST on Wednesday, February 11, 2026.

Members of the public and investors are invited to join the call and participate in the question and answer session by dialing 1 (800) 715-9871 (domestic) or 1 (646) 307-1963 (international) and using Conference ID 6226958, or via https://events.q4inc.com/attendee/958808765 by logging onto www.pega.com at least five minutes prior to the event's broadcast and clicking on the webcast icon in the Investors section.

Discussion of non-GAAP financial measures

Our non-GAAP financial measures should only be read in conjunction with our consolidated financial statements prepared in accordance with GAAP. We believe that these measures help investors understand our core operating results and prospects, which is consistent with how management measures and forecasts our performance without the effect of often one-time charges and other items outside our normal operations. Management uses these measures to assess the performance of the company's operations and establish operational goals and incentives. They are not a substitute for financial measures prepared under U.S. GAAP. Refer to the schedules at the end of this release for additional information, including a reconciliation of GAAP and non-GAAP measures.

Forward-looking statements

Certain statements in this press release may be "forward-looking statements” as defined in the Private Securities Litigation Reform Act of 1995, including our 2026 Guidance and the anticipated growth and development of our business.

Words such as expects, anticipates, intends, plans, believes, will, could, should, estimates, may, targets, strategies, intends to, projects, positions, forecasts, guidance, likely, and usually or variations of such words and other similar expressions identify forward-looking statements. These statements represent our views only as of the date the statement was made and are based on current expectations and assumptions.

Forward-looking statements deal with future events and are subject to risks and uncertainties that are difficult to predict, including, but not limited to:

These risks and others that may cause actual results to differ materially from those expressed in such forward-looking statements are described further in Part I of our Annual Report on Form 10-K for the year ended December 31, 2025, and other filings we make with the SEC.

Investors are cautioned not to place undue reliance on such forward-looking statements, and there are no assurances that the results included in such statements will be achieved. Although subsequent events may cause our view to change, except as required by applicable law, we do not undertake and expressly disclaim any obligation to publicly update or revise these forward-looking statements, whether as the result of new information, future events, or otherwise.

Any forward-looking statements in this press release represent our views as of February 10, 2026.

About Pegasystems

Pega provides the leading AI-powered platform for enterprise transformation. The world’s most influential organizations trust our technology to reimagine how work gets done by automating workflows, personalizing customer experiences, and modernizing legacy systems. Since 1983, our scalable, flexible architecture has fueled continuous innovation, helping clients accelerate their path to the autonomous enterprise. Ready to Build for Change®? Visit www.pega.com.

All trademarks are the property of their respective owners.

Our non-GAAP financial measures reflect the following adjustments:

(1) Per share amounts have been recast for all prior periods to reflect the effect of the Company’s two-for-one forward common stock split effected in the form of a stock dividend distributed on June 20, 2025.

(2) Stock-based compensation:

(3) Effective income tax rates:

Our GAAP effective income tax rate is subject to significant fluctuations due to several factors, including our stock-based compensation plans, research and development tax credits, and the valuation allowance on our deferred tax assets in the U.S. and U.K. We determine our non-GAAP income tax rate using applicable rates in taxing jurisdictions and assessing certain factors, including historical and forecasted earnings by jurisdiction, discrete items, and ability to realize tax assets. Under GAAP we recorded a release of our valuation allowance on our net deferred tax assets in the U.S. federal and state and U.K during the fourth quarter of 2025, resulting in a $175 million non‑cash tax benefit. See "Note 18. Income Taxes" in Part II, Item 8 of our Annual Report on Form 10-K for the year ended December 31, 2025 for additional information. We believe it is beneficial for our management to review our non-GAAP results consistent with our annual plan’s effective income tax rate as established at the beginning of each year, given tax rate volatility.

(1) Our non-GAAP free cash flow is defined as cash provided by operating activities less investment in property and equipment. Investment in property and equipment fluctuates in amount and frequency and is significantly affected by the timing and size of investments in our facilities and equipment. We provide information on free cash flow to enable investors to assess our ability to generate cash without incurring additional external financings. This information is not a substitute for financial measures prepared under U.S. GAAP.

(2) The supplemental information discloses items that affect our cash flows and are considered by management not to be representative of our core business operations and ongoing operational performance.

Annual contract value (“ACV”) - ACV represents the annualized value of our active contracts as of the measurement date. The contract's total value is divided by its duration in years to calculate ACV. ACV is a performance measure that we believe provides useful information to our management and investors.

Remaining performance obligations (“Backlog”) - Expected future revenue from existing non-cancellable contracts:

As of December 31, 2025:

As of December 31, 2024:

Cash Flow Growth

Total ACV Growth and Pega Cloud ACV Growth